Why Your Collections Technology Answers the Wrong Question (And What to Ask Instead)

Traditional collections platforms optimize for "who" and "when"—but miss the critical capability that actually drives recovery.

Key Takeaways

- Traditional collections technology excels at "who to contact" and "when"—but struggles with "how to motivate payment"

- This isn't a feature gap—it's an architectural limitation of analytics-first and workflow-first platforms

- Effective engagement requires behavioral segmentation, continuous experimentation, and closed-loop optimization

- Regulatory frameworks across US, UK, and Canada favor customer engagement approaches over pure enforcement

- Organizations seeing up to 25% improvement in recovery rates use fundamentally different architecture

The collections technology market has never been more crowded. Financial institutions, telcos, and utilities invest millions in decisioning engines, risk scoring platforms, and workflow orchestration tools. These platforms are sophisticated, well-engineered, and increasingly AI-powered.

Yet the data tells a troubling story: effective collection rates hover around 20% across comparable portfolios. Right Party Contact rates have declined to approximately 26% industry-wide. And 78% of debt collection companies report call blocking as a major operational challenge.

The technology isn't failing. It's solving the wrong problem.

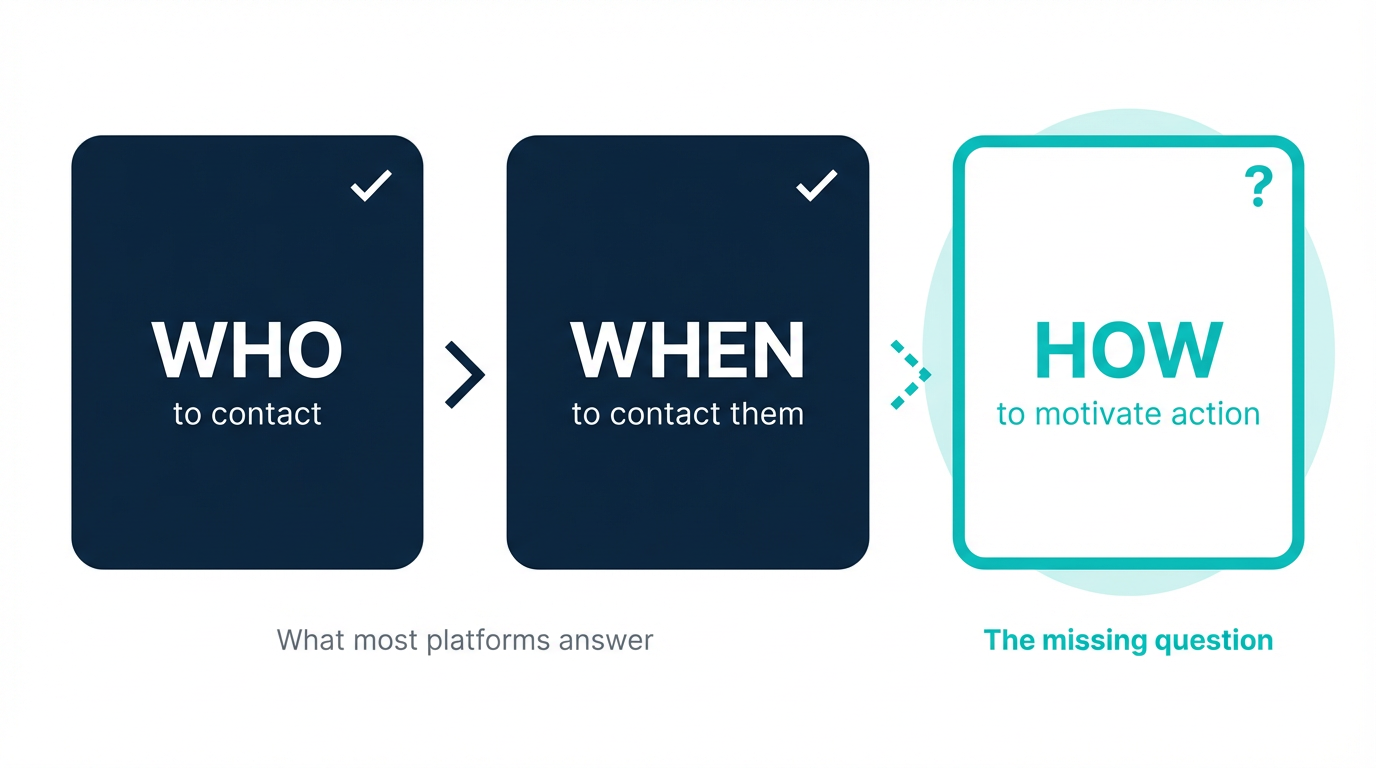

The Gap Between Knowing and Motivating

Traditional collections infrastructure excels at two questions: Who should we contact? and When should we contact them?

Risk scores predict probability of default with impressive accuracy. Workflow engines route accounts to the right queues at the right time. Analytics platforms segment customers by credit history, balance, and tenure.

But there's a third question these platforms struggle to answer: How do we motivate payment in a way that protects the customer relationship?

This isn't a feature gap. It's an architectural one.

Incumbent platforms are fundamentally analytics-first or workflow-first. They optimize for operational efficiency—routing the right accounts to the right queues at the right time—but lack explicit integration of behavioral economics principles that modern customer engagement demands.

The industry data confirms this gap matters: personalized approaches leveraging predictive analytics and behavioral modeling can significantly increase recovery rates, with some analyses indicating improvements of up to 25%.

Why "How to Motivate" Requires Different Infrastructure

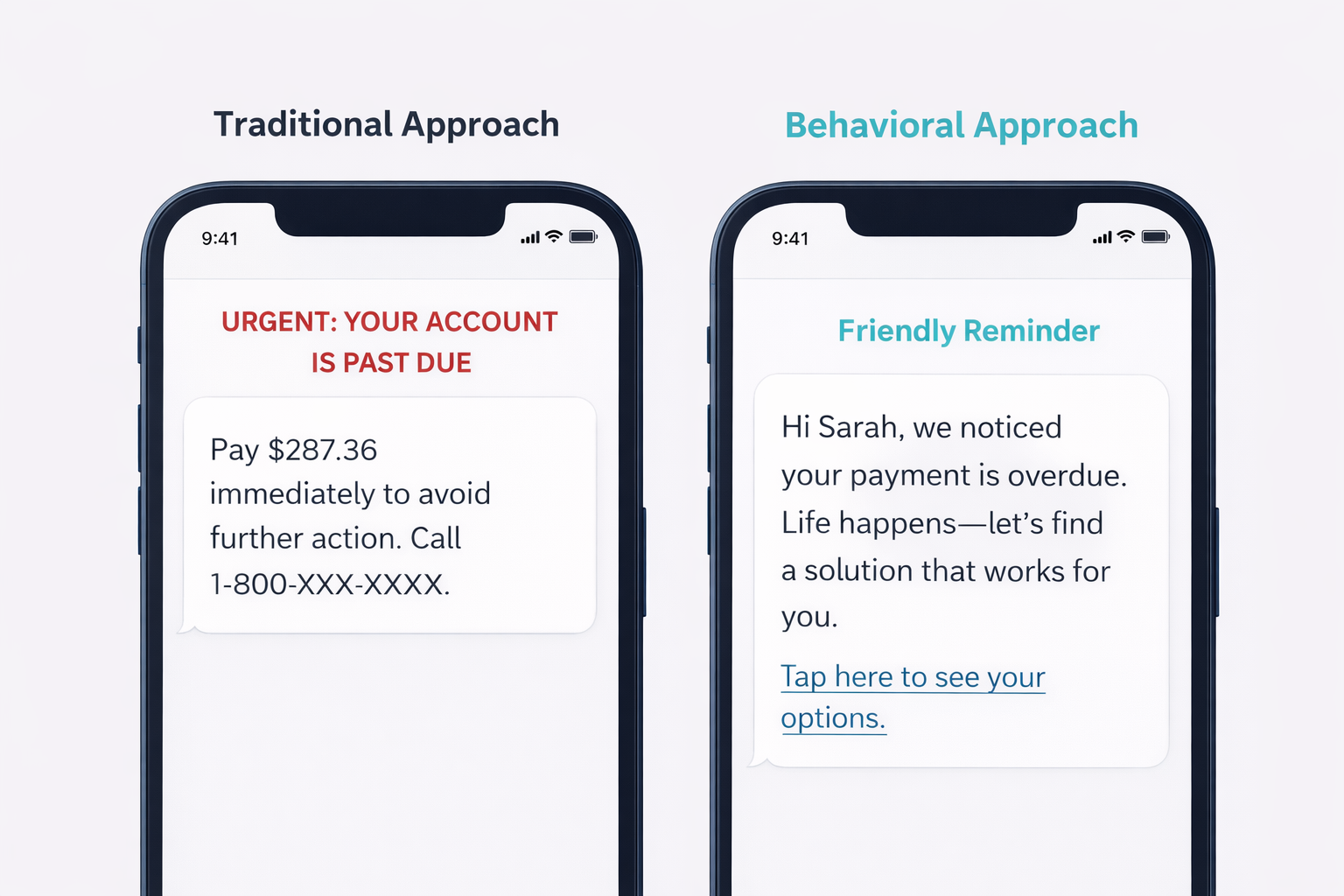

When customers are under financial stress, cognitive load increases dramatically. Research from Sendhil Mullainathan and Eldar Shafir on scarcity demonstrates that financial pressure functionally reduces decision-making capacity—a "bandwidth tax" that makes complex options harder to process.

This creates a compounding challenge: the customers who most need to engage with payment options are least equipped to navigate complex communication. Generic messages, rigid IVR menus, and one-size-fits-all contact strategies further increase friction.

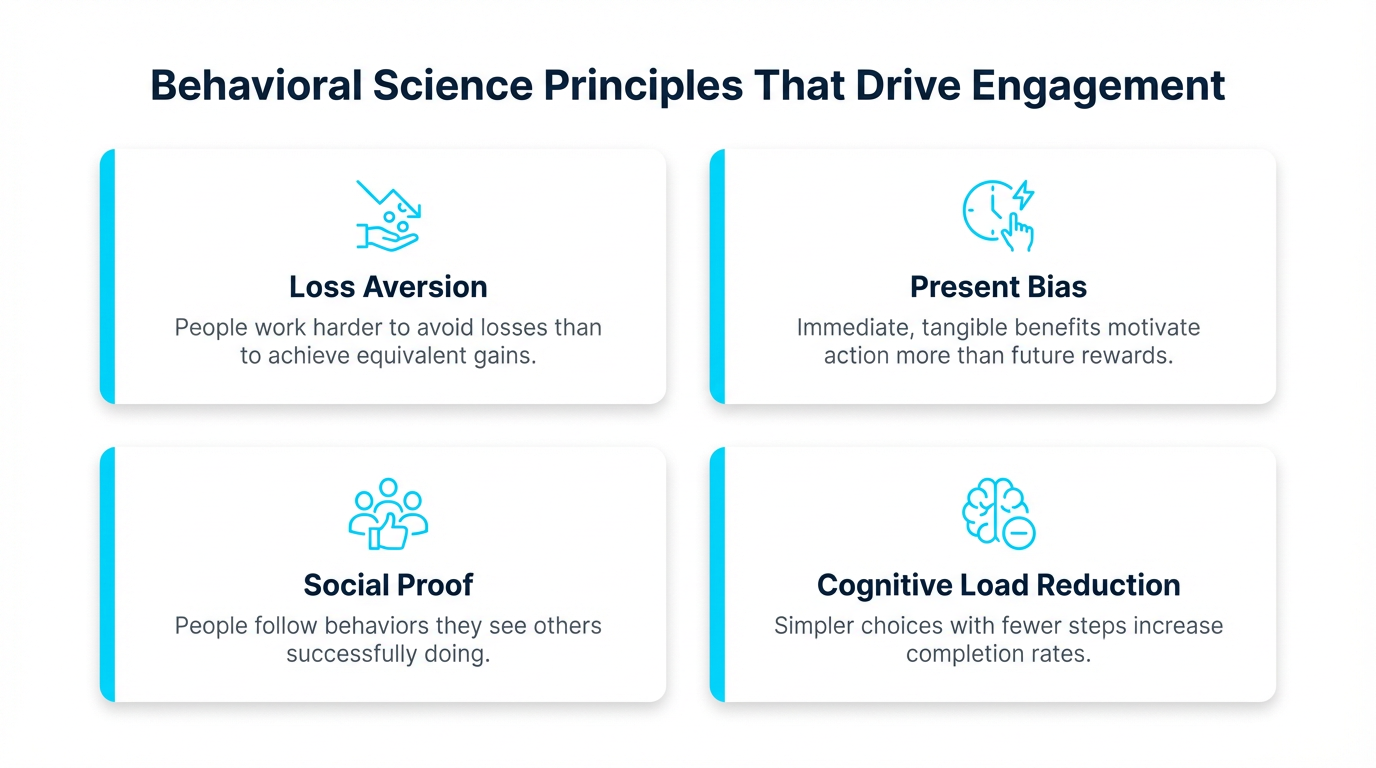

Effective engagement requires:

Behavioral Segmentation. Traditional collections segments customers by risk tier—how likely they are to default. But that misses the psychology. Behavioral segmentation distinguishes between customers who can't pay (facing genuine financial hardship) and customers who won't pay (capable but disengaged)—and identifies the specific mental shortcuts driving each. A customer avoiding their bills due to shame needs different messaging than one who's simply overwhelmed by too many choices.

Continuous Experimentation. Most platforms test messaging quarterly—run an A/B test, analyze results, implement changes. By the time insights reach production, customer behavior has shifted. Purpose-built systems test message framing, timing, and channel in real time, automatically learning from each interaction and adjusting the next outreach accordingly.

Closed-Loop Optimization. Contact rates and promise-to-pay metrics can mislead. A customer who answers every call but never pays isn't a success. Effective optimization measures what actually matters—payments made, customers cured, relationships preserved—and feeds those outcomes back into the system to refine future engagement.

General-purpose decisioning tools lack this specialized infrastructure. You can add behavioral nudges to an analytics platform, but you can't retrofit real-time experimentation onto architecture designed for batch processing.

The Regulatory Dimension

This capability gap has regulatory implications across North American and UK markets.

In the United States, the CFPB's Regulation F (implementing the Fair Debt Collection Practices Act) establishes requirements for how debt collectors communicate with consumers. The regulation governs validation notices, communication frequency, and the prohibition of harassment or deception.

In Canada, PIPEDA governs how personal information is collected and used in commercial activities, while provincial regulations like Quebec's Law 25 add additional privacy requirements. OSFI's guidelines establish expectations for managing operational risk in third-party arrangements, including collections technology.

In the United Kingdom, the FCA's Consumer Duty (effective July 2023) requires firms to "act to deliver good outcomes for retail customers." The April 2024 policy statement (PS24/2) strengthened protections for borrowers in financial difficulty.

Across all three jurisdictions, the regulatory trajectory favors approaches that treat collections as customer engagement rather than pure enforcement.

The Measurement Problem

Traditional collections metrics can obscure the gap between contact and motivation.

Consider promise-to-pay rates. A platform might report strong PTP numbers while actual conversion to payment remains weak. Surface-level metrics can improve while underlying economic outcomes do not.

Effective measurement requires outcome-based attribution: connecting specific communication approaches to actual payment behavior, then continuously optimizing based on what works.

What Different Architecture Looks Like

Platforms built on behavioral science methodology differ architecturally from analytics-first or workflow-first systems:

Data Foundation. Beyond credit data and account history, these platforms capture behavioral signals—engagement patterns, channel preferences, prior response—that inform personalized treatment.

Intelligence Layer. Propensity models predict not just risk, but readiness. Archetype classification identifies the psychological barriers to payment for each customer segment.

Engagement Engine. Message optimization happens at the individual communication level, testing framing, tone, and timing continuously.

Orchestration. Channels work together rather than in silos.

Measurement. Real-time dashboards track outcome-based metrics with clear attribution.

The key insight: behavioral science is the lens; AI is the horsepower that makes the methodology practical at enterprise scale.

The Integration Question

Organizations with significant investments in existing platforms face a practical question: does adopting behavioral engagement require replacing current infrastructure? The answer, in most cases, is no.

Behavioral engagement can function as a complementary layer—accepting risk signals from existing decisioning tools, executing optimized customer interactions, and returning behavioral intelligence to enrich enterprise data.

Moving Forward

Whether in financial services, auto financing, credit unions, telecommunications, or utilities—organizations facing rising delinquencies and constrained operating budgets need to ask: Are we investing in technology that answers the right question?

Who to contact and when matter. But without how to motivate, even the most sophisticated decisioning engine leaves significant value on the table.

The organizations seeing up to 25% improvement in recovery rates aren't just using better algorithms. They're using fundamentally different architecture—one that treats behavioral science as a core methodology, not a bolt-on feature.

Ready to ask the right question?

See how Symend's behavioral science-driven platform helps enterprises improve recovery rates while protecting customer relationships.

REQUEST A DEMOFrequently Asked Questions

Behavioral science-driven collections applies principles from behavioral economics and psychology to understand why customers in financial difficulty behave the way they do, then designs engagement strategies that motivate payment while preserving the customer relationship. Rather than relying solely on risk scores, it segments customers by capacity to pay and readiness to act.

Traditional risk scoring predicts the probability of default based on credit history and account data. Behavioral segmentation adds a psychological dimension—identifying whether a customer can't pay versus won't pay, and understanding the cognitive barriers driving their behavior. This creates actionable archetypes that inform different engagement strategies rather than just different contact frequencies.

Yes. Behavioral engagement typically functions as a complementary layer that accepts risk signals from existing decisioning tools like FICO or Experian, executes optimized customer interactions, and returns behavioral intelligence to enrich enterprise data.

Symend's framework identifies four archetypes: High Capacity/High Readiness (HCHR) customers who can pay and want to resolve quickly; High Capacity/Low Readiness (HCLR) customers who can pay but aren't motivated; Low Capacity/High Readiness (LCHR) customers who want to pay but face financial constraints; and Low Capacity/Low Readiness (LCLR) customers facing overwhelming financial stress.