The AI Collections Paradox: Why 70% of Companies Are Adopting Technology That May Be Driving Customers Away

How generic AI tools are undermining debt recovery—and the smarter approach that's delivering 6x higher cure rates.

Key Takeaways

- 70% of collections companies are adopting AI, but generic tools may actually be sabotaging recovery efforts

- Horizontal AI platforms lack understanding of the psychology behind debt repayment decisions

- The "ostrich effect"—where customers avoid rather than engage—is often triggered by generic AI messaging

- Behavioral science-informed AI delivers dramatically better results: 6x higher cure rates and 140% higher click-through rates

- Purpose-built solutions that combine AI with human intelligence create sustainable recovery outcomes

The rush to adopt AI in collections is accelerating. With delinquency rates climbing and operational costs under pressure, it's no surprise that 70% of collections companies are now exploring or actively implementing AI-powered tools. But here's the uncomfortable truth: generic AI may actually be sabotaging your recovery efforts.

The Allure—and Limits—of Horizontal AI

Platforms like AWS SageMaker, Google AI, Azure ML, ChatGPT, and Gemini offer impressive capabilities. They can analyze vast datasets, identify patterns humans might miss, and generate polished messages at scale. For collections teams looking to do more with less, the appeal is obvious.

But these horizontal AI tools share a critical flaw: they're designed for general purposes, not for the unique psychology of debt recovery. They don't understand how stress, emotions, and cognitive biases influence decision-making when customers are facing financial hardship.

The result? AI-generated outreach that looks efficient on paper but falls flat where it matters most—actually motivating customers to pay.

When AI Backfires: The "Ostrich Effect"

Consider three common AI-generated message types that seem reasonable but often trigger the opposite of the intended response:

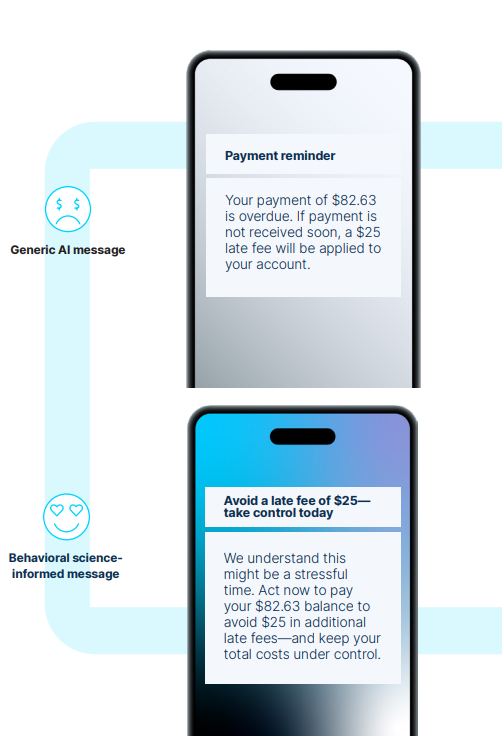

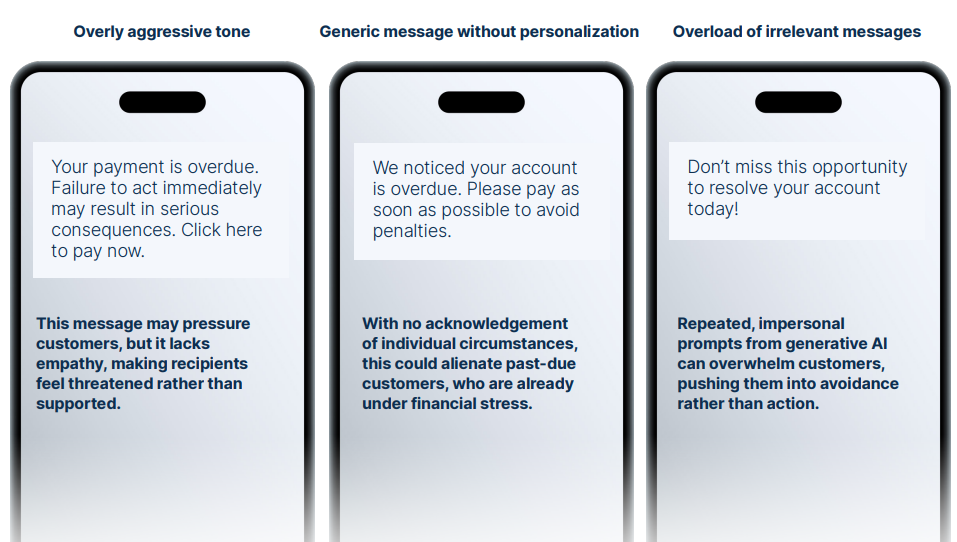

Overly aggressive: "Your payment is overdue. Failure to act immediately may result in serious consequences." This creates pressure but lacks empathy, making recipients feel threatened rather than supported.

Generic and impersonal: "We noticed your account is overdue. Please pay as soon as possible to avoid penalties." Without acknowledgment of individual circumstances, this alienates customers already under financial stress.

Message overload: Repeated, impersonal prompts can overwhelm customers, pushing them into avoidance rather than action—a phenomenon behavioral scientists call the "ostrich effect." This is why choice architecture matters so much in collections.

The Hidden Risks of DIY AI Segmentation

Beyond messaging, using generic AI for customer segmentation introduces serious risks that many teams overlook:

Compliance exposure: Training AI models on data points like age, race, or zip code can lead to discriminatory practices—and legal trouble. With generic platforms, the burden falls entirely on your team to prevent violations.

Amplified biases: If your training data is incomplete or skewed, models can reinforce unfair or ineffective segmentation, leading to strategies that systematically underperform for certain customer groups.

Missing behavioral context: Generic AI treats delinquent customers like data points. It can't account for the mental shortcuts people rely on when deciding whether to pay now, later, partially, or not at all.

The Trust Gap AI Can't Close Alone

Here's another challenge: consumer trust in AI is declining even as adoption increases. A Pew Research Center survey found that year-over-year, a growing number of people feel concerned rather than excited about AI in daily life.

For collections—where trust is often the foundation of repayment behavior—this creates a significant obstacle. If customers suspect they're interacting with an AI that doesn't understand their situation, even well-crafted messages can fall flat.

The Smarter Path: Behavioral Science-Informed AI

The solution isn't to abandon AI—it's to enhance it with human intelligence. Purpose-built solutions that integrate delinquency-specific behavioral science into segmentation and messaging deliver dramatically different results.

This approach combines AI's pattern recognition and scalability with insights into how people actually make decisions under financial stress. The result is outreach—whether through digital channels or conversational AI—that feels relevant, supportive, and aligned with customer needs.

Key behavioral principles that drive results:

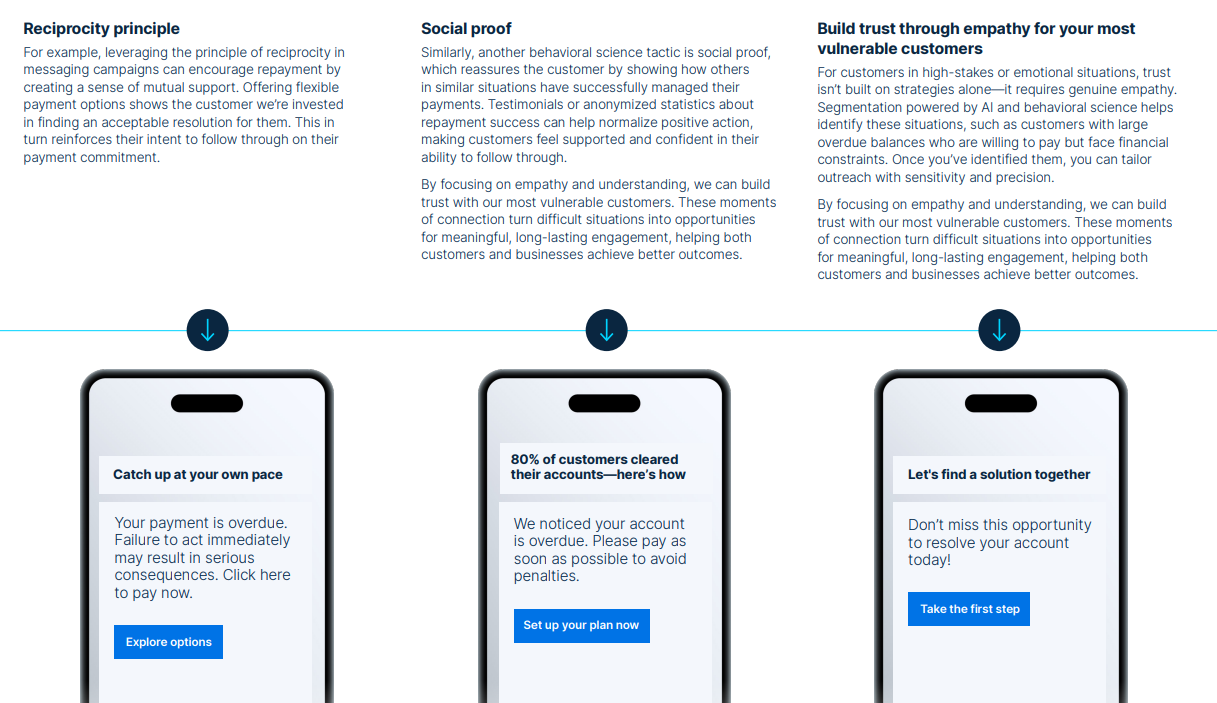

Reciprocity: Offering flexible payment options signals that you're invested in finding an acceptable resolution, which reinforces customers' commitment to follow through.

Social proof: Showing how others in similar situations have successfully managed payments normalizes positive action and builds confidence.

Empathy for vulnerable customers: For those with large overdue balances who are willing to pay but face constraints, sensitive outreach turns difficult situations into opportunities for long-term loyalty.

What Smarter Strategies Actually Deliver

When AI capabilities are combined with delinquency-focused behavioral science, the results speak for themselves:

These aren't theoretical projections—they're real outcomes documented in our case studies from strategies that address mental barriers, engage customers meaningfully, and motivate repayment behavior.

The Real Value: Customer Retention

Beyond immediate collection metrics, smarter strategies unlock long-term value. By building trust during challenging times, one-time resolutions become lasting customer relationships. Retaining customers rather than writing off debt strengthens your business sustainably.

The question isn't whether to use AI in collections—it's whether to use AI that understands the humans on the other end of every message.

Solutions like SymendCure combine AI with behavioral science to deliver hyper-personalized engagement that works across industries including financial services, telecommunications, and utilities.

Free eBook

Why Horizontal AI Harms Debt Recovery

Dive deeper into the risks of generic AI in collections and discover the behavioral science approach that's transforming recovery outcomes.

DOWNLOAD THE EBOOKFrequently Asked Questions

Unlike horizontal AI platforms designed for general-purpose applications, Symend's AI is purpose-built for debt recovery. Our platform integrates delinquency-specific data with behavioral science principles from the ground up—not as an afterthought. This means our AI understands the psychological factors that influence repayment decisions, such as financial stress, cognitive biases, and emotional barriers. Generic AI can process data and generate messages, but it can't account for why a past-due customer might avoid contact or delay payment. Symend's AI does.

Behavioral science is the study of how people actually make decisions—not how we assume they should. In collections, this means understanding that customers under financial stress often rely on mental shortcuts and coping mechanisms that generic outreach ignores. Symend applies proven behavioral principles like reciprocity (showing flexibility to encourage commitment), social proof (demonstrating that others in similar situations have resolved their accounts), and loss aversion (framing messages around what customers can protect rather than what they'll lose). These insights are embedded directly into our segmentation and messaging strategies.

Organizations using Symend's behavioral science-informed AI consistently see measurable improvements: 10X ROI, 10% or more increase in recovery rates, and up to 50% reduction in operational costs through intelligent automation. Our approach also improves customer retention—turning difficult moments into opportunities for long-term loyalty rather than write-offs.

Compliance is built into our platform, not bolted on. Symend's AI is designed to avoid discriminatory practices by excluding protected data points from segmentation models. We maintain compliance with regulations across the US, UK, and Canada, including FDCPA, TCPA, Reg F, and regional consumer protection laws. Unlike DIY approaches with generic AI—where your team bears full responsibility for compliance—Symend provides guardrails that help protect your organization from regulatory risk.

Yes. Symend is designed to integrate with your existing tech stack and enhance your current operations rather than replace them. Our platform can augment your in-house collections efforts, work alongside your existing communication channels, and provide insights that improve both automated and agent-assisted interactions. Many organizations start by deploying Symend for specific customer segments or stages of delinquency, then expand as they see results.