Past-due customers don't all ignore you for the same reason. Symend's Delinquency Archetypes framework identifies the behavioral profile behind each account — so engagement is designed to change behavior, not just reach it.

See It in ActionMost collections platforms segment accounts on a single axis: days past due. A 30-day account gets one treatment; a 60-day account gets another. It's simple, auditable, and fundamentally insufficient.

Days past due measures elapsed time, not behavior. It tells you how long a customer hasn't paid — but nothing about why. And the why is the only thing that determines what will make them pay.

Two accounts at 45 days past due can represent completely opposite situations. One customer has the money and just needs a clear, frictionless path to resolution. Another is overwhelmed by financial stress with severely narrowed cognitive bandwidth — and every escalating call makes them less likely to engage. Treating them identically guarantees suboptimal outcomes for both.

Behavioral science research on payment psychology shows the real segmentation axis isn't time — it's a combination of financial capacity and psychological readiness. That's the foundation of Delinquency Archetypes.

Delinquency Archetypes classifies every past-due customer on two independent dimensions. Each dimension answers a different question — and both must be understood before the right engagement strategy can be designed.

The competitive advantage isn't AI — everyone has that now. It's knowing which behavioral mechanism is preventing payment, and designing the engagement to address it precisely.

The framework isn't a reporting layer — it's the decisioning layer. Archetype classification runs at the account level before every contact, dynamically adapting channel, message, timing, and offered options to match each customer's behavioral profile in real time.

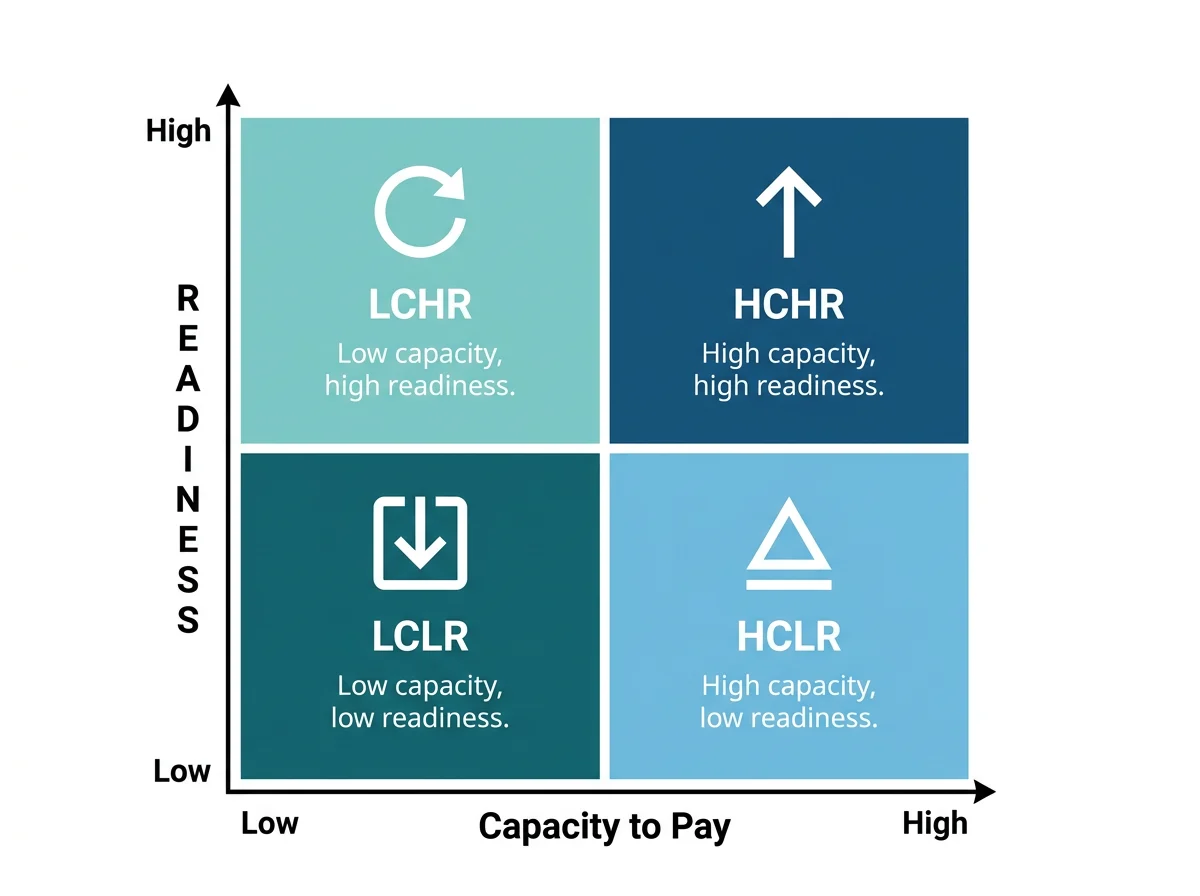

Delinquency archetypes are a behavioral science-based segmentation framework developed by Symend that classifies past-due customers by two dimensions: capacity to pay (their financial ability) and readiness to act (their psychological readiness to take action). The framework produces four distinct profiles — HCHR, HCLR, LCHR, and LCLR — each driven by a different behavioral mechanism and requiring a fundamentally different engagement strategy. Unlike traditional risk scoring, which segments solely on financial probability, Delinquency Archetypes capture the motivational and behavioral context that determines how a customer will respond to outreach.

The Delinquency Archetypes framework is Symend's proprietary 2x2 segmentation model built on two independent axes: capacity to pay (can the customer afford to pay?) and readiness to act (is the customer psychologically ready to take action?). Each quadrant maps to a specific behavioral profile — the HCHR customer who just needs a clear, frictionless path; the HCLR customer whose complacency requires urgency-without-pressure; the LCHR customer who is motivated but needs flexible options; and the LCLR customer who is overwhelmed and needs a single, simple next step rather than a menu of choices. The framework emerged from behavioral science research on how financial stress, cognitive load, and decision-making psychology shape payment behavior in ways that days-past-due scores cannot capture.

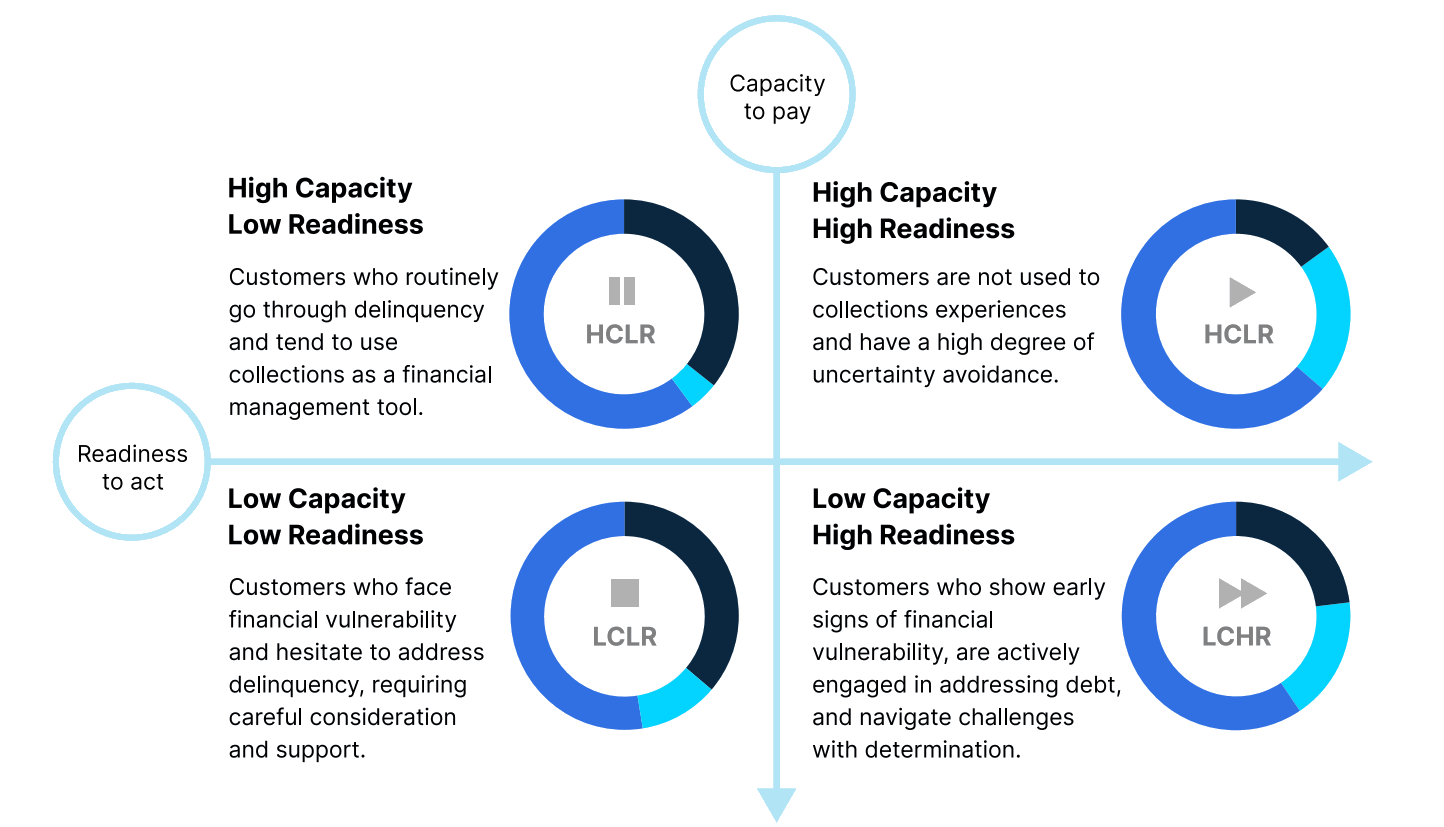

The four Delinquency Archetypes are: (1) HCHR — High Capacity, High Readiness: can pay and wants to resolve; driven by uncertainty avoidance; needs a fast, frictionless path to payment. (2) HCLR — High Capacity, Low Readiness: can pay but isn't motivated; driven by the Decision from Experience Gap — repeated late payments without consequence creates complacency; needs urgency reframing without feeling pressured. (3) LCHR — Low Capacity, High Readiness: wants to pay but genuinely can't in full; driven by goal approach motivation; needs flexible payment arrangements and affirming, supportive communication. (4) LCLR — Low Capacity, Low Readiness: experiencing significant financial stress with severely narrowed cognitive bandwidth due to tunneling; needs early, empathetic intervention with a single, simple next action rather than a menu of options.

Credit risk scoring answers one question: how likely is this customer to pay? Behavioral segmentation answers a different question: why aren't they paying, and what will actually move them to act? A high-risk score can be shared by two customers with completely opposite behavioral profiles — one who is financially capable but complacent (HCLR), and one who is motivated to pay but genuinely cannot afford to do so right now (LCHR). Treating them the same way — same channel, same message, same urgency — will work for neither. Behavioral segmentation on capacity AND readiness produces distinct profiles that map directly to distinct engagement strategies, which is why platforms using behavioral archetypes consistently outperform risk-score-only systems on recovery rate and cost-to-collect.

Capacity to pay refers to whether a customer has the financial means to make a payment — it is a measure of economic ability. Readiness to act refers to whether a customer is psychologically prepared and motivated to take action on their debt — it is a measure of behavioral willingness. These two dimensions are independent of each other. A customer can have high capacity (the money is there) but low readiness to act (they're avoiding, rationalizing, or procrastinating). Equally, a customer can have low capacity (genuinely stretched) but high readiness to act (they want to resolve it and are actively looking for options). Segmenting on both axes simultaneously is what enables collections engagement to be both precise and empathetic — and it's why behavioral segmentation consistently outperforms single-axis risk scoring on actual recovery outcomes.

LCLR customers — Low Capacity, Low Readiness — are experiencing what behavioral scientists call tunneling: financial stress narrows cognitive bandwidth, making it harder to process options, plan ahead, or take action. Standard collections approaches that present multiple options, long-form messages, or escalating urgency make this worse by adding to cognitive load. Effective LCLR engagement focuses on bandwidth expansion: one simple, clearly framed action (not a list of options), empathetic language that acknowledges difficulty without blame, a concrete and achievable next step such as a small payment arrangement rather than a full balance demand, and channel selection that reaches them without triggering avoidance behaviors. Earlier outreach in the delinquency cycle — before multiple missed payments compound the financial stress — is generally more effective for this archetype than later-stage escalation.

Uniform collections outreach — same message, same channel, same frequency for all past-due accounts — is optimized for none of the behavioral profiles that actually exist in a delinquent portfolio. The HCHR customer self-cures quickly with minimal prompting; over-engagement wastes cost without improving outcome. The HCLR customer requires urgency reframing that generic reminders don't provide. The LCHR customer needs flexible options that standard demand letters don't offer. The LCLR customer disengages when faced with high-pressure or complex messaging. Industry research suggests more than three-quarters of outbound collection calls are blocked or ignored — evidence that uniform outreach is already being filtered out at scale. Recovery rates stagnate precisely because more of the same approach reaches the same accounts in the same ineffective way.

Enterprise organizations using Symend's Delinquency Archetypes framework have achieved: 60%+ cure rate lift (UK credit card provider), 26.6% self-cure rate (Rifco auto finance), 85% reduction in agent interactions, up to 10% increase in overall recovery rates, and 220% increase in digital engagement (TELUS). These outcomes reflect a core principle: effort concentrated where interventions will actually change behavior — on accounts where the right engagement approach can shift the outcome — outperforms distributed effort applied uniformly across all accounts regardless of behavioral profile.

Talk to our team about how archetype-driven engagement can improve recovery rates and reduce cost-to-collect across your portfolio.

Get a Demo Read the methodology →Because keeping customers is as important as recovering debt.