Delinquency Management: Why Predictive AI Alone Isn't Enough

The gap between contact efficiency and engagement effectiveness is where effective delinquency management lives

Key Takeaways

- Delinquency management is the end-to-end process of identifying and resolving past-due accounts through proactive engagement — not just pursuing payment after the fact.

- Predictive AI tells you who is at risk and when to contact them — but not why they aren't paying or what will motivate them to act.

- Generic AI tools often deliver an "Initial Bump" — short-term gains that plateau once contact efficiency maxes out, without changing customer willingness to pay.

- Behavioral science provides the missing layer: a framework that classifies customers into four Delinquency Archetypes based on capacity and readiness to pay, enabling truly personalized intervention.

- AI and behavioral science work best together: AI operates at scale, behavioral science determines the right message for each psychological profile.

Every major platform vendor now offers a collections AI solution. They promise smarter segmentation, optimized contact timing, and reduced agent workload. And many of them deliver real improvements — particularly in the early stages of deployment.

But here is the challenge most enterprise collections leaders eventually run into: the results plateau. Contact rates improve, then stagnate. Recovery lifts initially, then flattens. The AI has done what it was built to do — reach more people, faster. What it was not designed to do is tell you why those people are not paying, or what would actually change their behavior.

That gap — between contact efficiency and engagement effectiveness — is where effective delinquency management lives. This post explains why, and what filling that gap requires.

What Is Delinquency Management?

Delinquency management is the proactive process of identifying at-risk accounts early and engaging customers through personalized, behaviorally-informed outreach before debt escalates to third-party collections or write-off. Unlike reactive collections — which pursue payment after significant account degradation — delinquency management prioritizes resolving early-stage arrears while preserving the customer relationship. It spans financial services, telecoms, utilities, and auto finance.

The distinction from traditional debt collection matters. Traditional collection is reactive — it kicks in after an account has already degraded significantly. Delinquency management is upstream. The goal is to keep customers in good standing, resolve early-stage arrears before they compound, and preserve the customer relationship in the process.

This upstream orientation is relevant across every industry where recurring billing drives revenue — financial services, telecommunications, utilities, and auto finance. In each of these verticals, a past-due account is not just a balance to be recovered; it is a customer relationship at risk of permanent loss.

Why Traditional Collections Approaches Often Fail

Risk scores are necessary — but they only answer half the question

Traditional delinquency platforms segment customers by risk score, outstanding balance, and days past due. This tells you who might not pay. It does not tell you why — and without the why, you cannot design an effective intervention.

A customer with a high risk score and a $400 balance might be someone who genuinely cannot afford to pay this month. Or someone who is habitually late but will pay when prompted. Or someone who has mentally written off the debt because they feel overwhelmed. Identical risk profiles, completely different behavioral situations, and completely different optimal responses.

Basic risk segmentation is limited precisely because it does not incorporate any real-time behavioral information gathered through the process of actually engaging with customers. It is a static snapshot in a dynamic situation. For a deeper look at why generic AI approaches fall short in collections, see Why Horizontal AI Harms Debt Recovery.

The Initial Bump Trap

When organizations deploy generic AI collections tools, they typically see an early lift. Automation reaches more customers faster, the dial-up on contact volume produces more responses, and recovery numbers improve. Leadership is encouraged.

Then the curve flattens.

The AI has optimized for contact efficiency — it is reaching as many people as it can, as efficiently as possible. But it has not changed the underlying psychological barriers to payment. Customers who were not motivated to engage before are still not motivated to engage. The system has run out of runway because contact optimization alone does not address the underlying behavioral barriers to payment. Approaches that layer behavioral science onto AI — such as archetype-driven segmentation and nudge-level message optimization — have been shown to help organizations break through this ceiling.

One-size-fits-all outreach drives avoidance

When every past-due customer receives the same message — the same tone, the same framing, the same urgency level — the outreach stops feeling relevant and starts feeling like noise. Customers who need empathetic support to navigate genuine hardship feel pressured and disengage. Customers who would respond to a clear, low-friction nudge receive the same heavy-handed script as everyone else.

Research across 3,514 participants in 11 European countries found that financially distressed individuals consistently describe interactions with traditional collections as adversarial, dignity-reducing, and counterproductive to resolution. The industry's own tools are reinforcing the avoidance behavior they are trying to overcome.

The Missing Layer: Behavioral Science

Behavioral science improves delinquency management by identifying the specific psychological barrier preventing each customer from paying — scarcity mindset, avoidance, complacency, or uncertainty — and matching that customer to the intervention most likely to change their behavior. This requires purpose-built models grounded in psychological research, validated across millions of delinquency interactions. General-purpose AI platforms do not provide this layer.

This is not something a general-purpose AI platform provides. It requires purpose-built models grounded in psychological research and validated across millions of real customer interactions. The frameworks that matter here — the scarcity mindset, loss aversion, the Capability-Opportunity-Motivation model, mental accounting — each predict different customer behaviors and require different interventions. Misdiagnosing the cause of non-payment and applying the wrong intervention makes outcomes worse, not better.

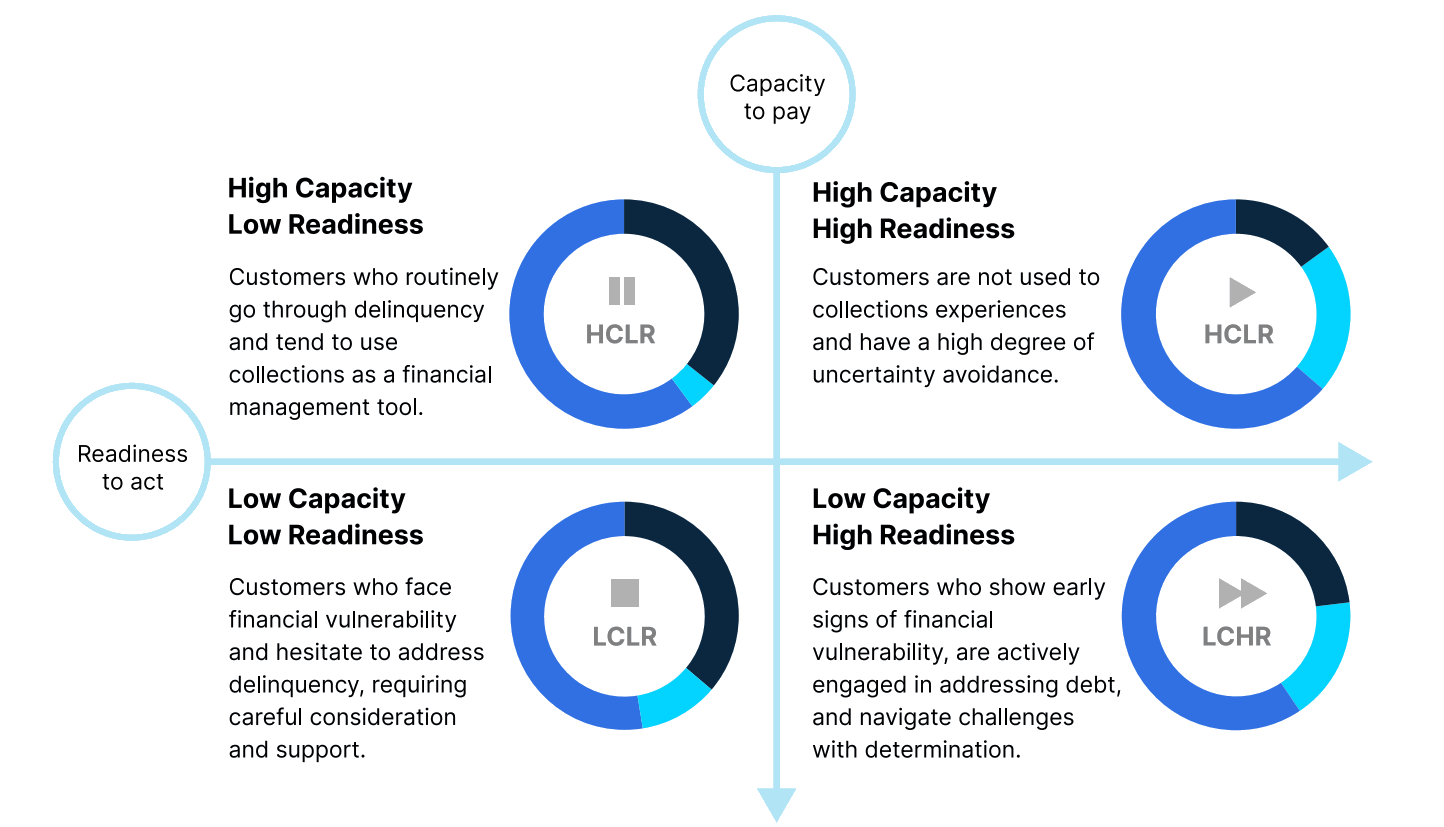

Delinquency Archetypes: a dual-axis behavioral framework

Symend's Delinquency Archetypes framework classifies past-due customers along two behavioral dimensions: capacity to pay and readiness to engage. The result is four distinct archetypes, each with a different psychological profile, different motivational drivers, and a different optimal intervention strategy.

| Archetype | Profile | What Drives Them | Effective Intervention |

|---|---|---|---|

| HCHR | Can pay and willing to engage | Uncertainty avoidance — they want clarity on what they owe and how to resolve it quickly | Provide clear, empathetic information; remove friction so they can resolve immediately |

| HCLR | Can pay but not engaging | Decision from Experience Gap — repeated late payments without consequence creates complacency | Reframe the risks of habitual delinquency; counter the assumption that delay is cost-free |

| LCHR | Limited means but willing | Goal approach — striving toward resolution, motivated but constrained | Affirm their effort, celebrate small steps, offer payment arrangements that feel achievable |

| LCLR | Limited means and disengaged | Tunneling amid scarcity — overwhelmed by financial stress, cognitive bandwidth severely narrowed | Expand cognitive bandwidth; present single, simple, actionable next steps — not a menu of options |

Treating all four archetypes the same — as traditional risk-score-only systems do — wastes effort on HCHR customers who simply need a clear nudge, while simultaneously failing the LCLR customers who need a fundamentally different approach. The segmentation is not just more precise; it is more human.

"The competitive advantage isn't AI — everyone has that now. It's the science behind the decisions."

How Predictive AI and Behavioral Science Work Together

Predictive AI and behavioral science work together in enterprise collections by dividing responsibilities: AI identifies which accounts are at risk, determines optimal contact timing and channel at scale, and processes behavioral signals no human team could monitor manually. Behavioral science then determines what to say and how to frame it — which motivational lever moves a specific customer archetype from avoidance to action.

Predictive AI identifies which accounts are at risk, determines the optimal timing and channel for each contact, and processes the volume of signals that no human team could monitor manually. But on its own, AI can tell you that a customer is at risk — it cannot tell you what that customer is thinking, what barrier is preventing them from acting, or what framing will change their behavior.

Behavioral science provides the strategy that AI executes. It determines what to say, how to frame it, and what motivational lever is most likely to move a specific customer type from avoidance to action.

The combination works like this in practice: predictive scoring identifies a customer as HCLR — high capacity, low readiness. Behavioral science determines that this archetype is driven by a Decision from Experience Gap: they have been late before without serious consequence, so they underestimate the risk of being late again. The intervention is not a payment reminder. It is a message that reframes the cumulative risk of habitual delinquency in terms that are personally relevant to this customer. The AI delivers it through the right channel, at the right time, at scale across hundreds of thousands of accounts.

The AI capabilities that make behavioral science scalable

Several AI capabilities are critical to making behavioral science work at enterprise scale:

- Predictive scoring for archetype identification — supervised machine learning trained on hundreds of millions of delinquency interactions, identifying which archetype a customer belongs to and when their readiness is likely to shift

- Reinforcement learning for journey optimization — continuously refining the engagement sequence for each archetype based on incoming interaction data, without human intervention

- NLP for sentiment analysis — analyzing customer responses to understand emotional state and refine archetype classification in real time

- Advanced experimentation for message optimization — more sophisticated than basic A/B testing, advanced multi-armed optimization algorithms test specific behavioral nudges within communications and automatically allocate traffic toward better-performing variants

What to Look for in a Delinquency Management Platform

If you are evaluating delinquency management software, predictive AI capability should be considered table stakes — not a differentiator. The questions that matter are about the behavioral layer on top of it. For a broader look at which AI capabilities actually deliver results — and which ones plateau — see AI in Debt Collections: What Works, What Doesn't in 2026.

-

Behavioral segmentation, not just risk scoring

Does the platform segment by capacity to pay AND readiness to engage? Or does it only work from risk score and balance? The former enables genuinely differentiated interventions. The latter is a more sophisticated version of the same approach that has been producing plateau results for years.

-

Archetype-level optimization

Can you test and refine specific behavioral nudges for different customer archetypes? The ability to run targeted experiments within archetype segments — rather than portfolio-wide A/B tests — is what separates a behavioral platform from a contact-automation platform.

-

Integrated platform vs. fragmented stack

Stitching together separate tools for CRM, decisioning, AI scoring, communications, and analytics introduces costly complexity, slows learning velocity, and creates data gaps between systems. An integrated platform ensures that every interaction feeds the same behavioral model.

-

Continuous learning — not just periodic model updates

Customer behavior evolves. Channel preferences shift. Macroeconomic conditions change. A static behavioral model degrades over time. The platform should use techniques like advanced optimization techniques — not just basic A/B testing — to continuously optimize engagement at the nudge level in real time.

-

Empathetic engagement design

Does the platform de-escalate and guide customers toward resolution, or does it simply automate contact at higher volume? The tone, framing, and psychological design of every communication should be driven by behavioral science — including AI-powered conversational engagement that can respond to customer intent in real time.

-

Glass-box explainability

Can you trace exactly why any decision was made — which signals drove an archetype classification, why a specific message was selected, what outcome it produced? Regulators across financial services, utilities, and telecommunications are increasingly focused on AI governance and the ability to audit decisioning. A black-box model is a compliance liability. Read more about glass box vs. black box AI governance.

Real-World Results

The impact of combining behavioral science with AI is visible in the outcomes Symend has produced across enterprise clients in financial services, telecommunications, and auto finance.

For full case study details, see the Rifco case study and explore Symend's results in telecommunications, banking and financial services, and utilities.

"Symend actually helped us see our collections strategy a little bit differently. We don't necessarily have to do the same thing at the same frequency on every account every day. AI couldn't have shown us that."

— Tammy Shanks, Manager of Collections and Customer Service, Rifco

The Bottom Line

Delinquency management is evolving — from "contact more people faster" to "understand each person and engage them appropriately." The organizations getting this right are not just recovering more; they are retaining more customers, reducing operational cost, and building brand equity in interactions that used to destroy it.

The competitive advantage is no longer AI. AI is a commodity. The advantage is the science behind the decisions: understanding why a customer is not paying, knowing what type of engagement will change their behavior, and having the continuous learning infrastructure to improve over time.

That combination — behavioral science and AI working together — is what effective delinquency management requires in 2026.

Ready to go beyond contact efficiency?

See how SymendCure combines behavioral science with AI to drive sustainable recovery — or download the Future of Collections Technology white paper for a deeper look at how behavioral science and AI are shaping the future of enterprise collections.

REQUEST A DEMO