7 Behavioral Science Tactics That Determine Whether a Customer Pays or Ignores You

The 7 behavioral science tactics that drive — or block — repayment, with real before-and-after message examples from 250M+ delinquency treatments.

Key Takeaways

- The industry has invested billions in knowing who to contact and when, but very little in what the message actually says — and the message is what drives action.

- Seven behavioral tactics consistently move customers from inaction to resolution: loss aversion, temporal discounting, simplicity bias, social herding, the endowment effect, anchoring, and ease framing.

- A 13-million-person field study published in PNAS (January 2025) found behaviorally-informed messages reduced 60-day delinquencies by 0.42 percentage points — an estimated 79,800 delinquencies averted at full scale.

- Applied together, the seven tactics compound: every phrase in a well-designed message can be doing psychological work simultaneously.

- Symend's platform has applied these tactics across 250+ million delinquency treatments and recovered more than $50 billion, with up to 10% higher recovery rates, 152% engagement lift, and 85% fewer agent interactions versus legacy approaches.

Picture two customers. Both are 30 days past due. Both have the money sitting in their checking account. One pays within hours of receiving a message. The other ignores it completely.

The difference isn't income. It isn't intention. It isn't even the channel the message arrived on.

It's the behavioral science tactics that were — or weren't — accounted for in the message they received.

This is the variable the collections industry has systematically ignored. Billions have been invested in AI scoring models, channel optimization, and contact-rate technology. But the message itself — the actual words a past-due customer reads or hears — has largely been left to intuition, legal review, and legacy templates written a decade ago. This guide breaks down 7 of the behavioral science tactics most relevant to debt recovery, with real before-and-after message examples and a practical framework for operationalizing each one.

Why Behavioral Science Is the Variable Nobody Controls For

The collections industry has gotten very good at determining who to contact and when. It has invested heavily in predictive scoring, channel optimization, and AI-driven account prioritization. 57% of AI adopters in collections now use AI specifically to predict and segment accounts and forecast payment outcomes (Bridgeforce, 2025).

And yet contact rates remain stubbornly low. Fewer than 20% of outbound collection contacts actually reach a customer — and even among those reached with money to pay, many don't act. The missing variable isn't who or when. It's what to say and how to say it — the message design, framing, and psychological architecture that determines whether a customer engages when the message arrives.

Symend has treated over 250 million delinquencies and recovered more than $50 billion using a platform built on behavioral science, not just AI scoring. The behavioral science is the reason. This guide is a breakdown of how it works at the message level.

"The industry has invested billions in knowing who to contact and when. It has barely invested in understanding why the message fails when it arrives."

The 7 Behavioral Science Tactics — And How to Use Them

Each tactic below follows the same format: what it is, why it matters in collections, what a traditional collections message looks like, what a behavioral science-driven message looks like, and how to operationalize it at scale. These tactics are drawn from Symend's own behavioral tactics library, refined across 250+ million treated delinquencies.

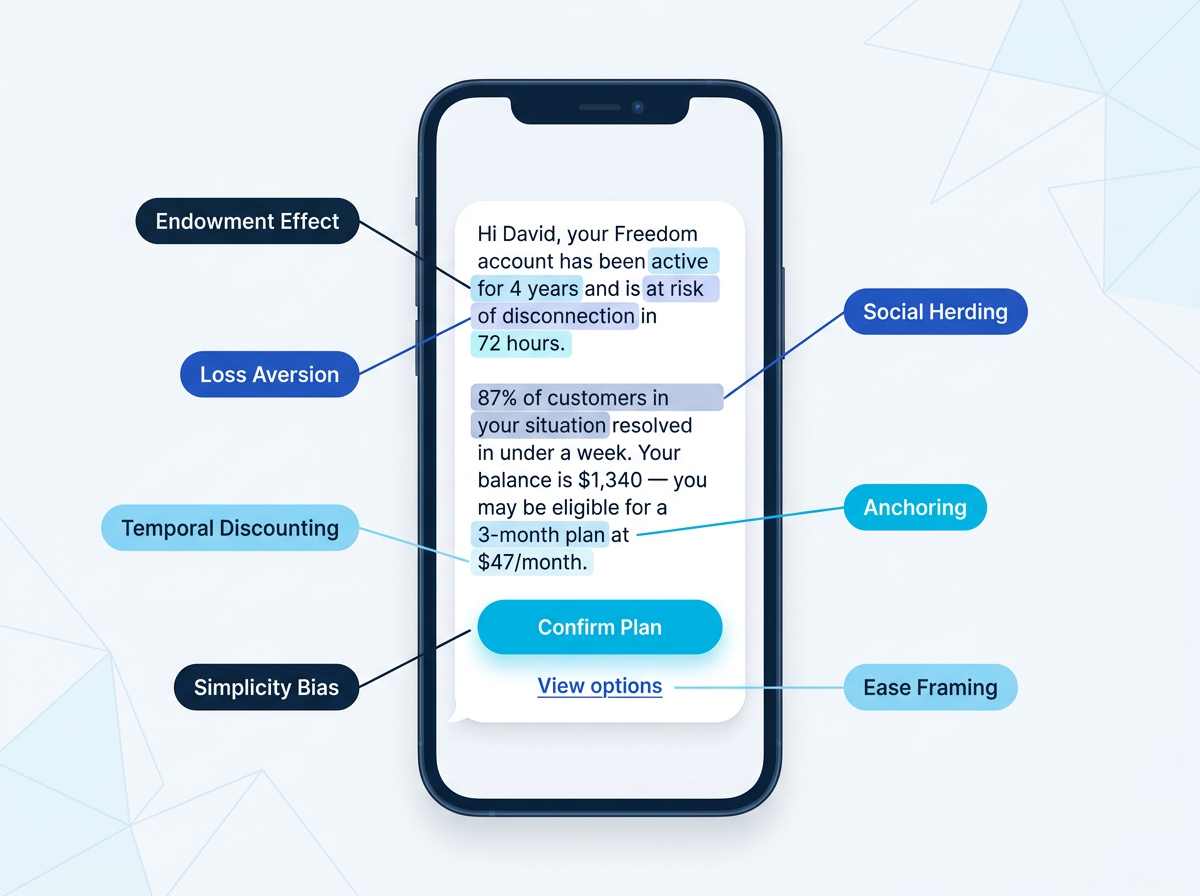

Tactic 1: Loss Aversion

What it is: People experience the pain of a loss roughly twice as intensely as the pleasure of an equivalent gain — one of the most replicated findings in behavioral economics, established by Kahneman and Tversky's Prospect Theory.

Why it matters: Most collection messages are framed around positive outcomes — restoring service, clearing a balance, returning to good standing. These are gains. But customers respond far more powerfully to what they stand to lose: credit scores, service access, financial relationships built over years.

Operationalize it: Lead every message with the specific loss at stake. Name it concretely — not "account issues" but "service disconnection" or "credit score impact." Use the verbs protect, keep, preserve rather than get, earn, restore.

Tactic 2: Temporal Discounting

What it is: Humans systematically value money in the present more than money in the future — and find it less stressful to commit to paying later than to pay now. The pain of paying today feels greater than the abstract pain of collections action next month, even when the math says otherwise.

Why it matters: Traditional messages lean heavily on future consequences — referral to collections, credit damage, eventual escalation. These are real, but they're temporally distant enough that temporal discounting blunts their impact. Pair temporal discounting awareness with the urgency tactic to collapse the distance between message and action.

Operationalize it: Make the reward of resolving now feel immediate and concrete. Use real-time framing ("updates immediately," "flag removed today"). Attach specific near-term deadlines — not "soon" but "Thursday at 11:59 PM."

Tactic 3: Simplicity Bias

What it is: People prefer simple explanations and solutions over complex ones, even when the complex option may be more accurate. This is rooted in the cognitive ease of processing simple information — and it compounds dramatically under financial stress, which measurably reduces cognitive bandwidth.

Why it matters: Symend's 2023 consumer research found that while 60% of past-due customers value flexibility in managing their balance, 54% specifically want solutions that fit their needs, not an undifferentiated menu (Symend Decoding Billpayer Behavior Report, 2023). Pair simplicity bias with the clarity tactic: every option presented should be clean, scannable, and free of unnecessary complication.

Operationalize it: Present a maximum of two to three options. Pre-select the recommended one. Use progressive disclosure — lead with the single best choice, and let the customer opt into complexity if they want it.

Tactic 4: Social Herding

What it is: In uncertain situations, people look to the behavior of similar others to calibrate their own decisions. Information about what comparable peers are doing functions as a powerful form of normative social influence — one of the most reliable drivers of behavior change identified in Robert Cialdini's foundational research on influence.

Why it matters: Past-due customers often feel isolated — as if they're the only person in this situation, facing judgment from a faceless institution. Social herding breaks that isolation and normalizes the act of resolving the debt.

Operationalize it: Use peer references based on behavioral segments, not account categories. Cite resolution rates, not delinquency rates. Symend's delinquency archetypes framework makes precision social herding operationally feasible at scale — a high-capacity, high-readiness customer hears different peer comparisons than a low-capacity, low-readiness customer, because the relevant "herd" is different.

Tactic 5: The Endowment Effect

What it is: People overvalue things they already own, regardless of market value. The pain of losing something owned exceeds the pleasure of acquiring something equivalent — a finding repeatedly demonstrated in Daniel Kahneman's endowment effect research.

Why it matters: Collections messaging typically frames the customer as needing to restore something they've lost. But if the account is still active — even 30 days past due — the customer still owns that relationship, that credit history, that tenure. Framing messages around protecting what they already have triggers the endowment effect significantly more powerfully than framing them around restoration.

Operationalize it: Reference tenure explicitly — years as a customer, payment history, account standing. Frame credit scores as possessions to protect. Use ownership language: your account, your history, what you've built.

Tactic 6: Anchoring

What it is: When making decisions under uncertainty, people anchor on the first number that comes to mind and adjust away from it. The anchor biases the decision even when the person knows it shouldn't. A full balance shown first makes a monthly payment feel small by comparison. A minimum payment shown first — with no context — feels arbitrary or inadequate.

Why it matters: Most collections messages either lead with the minimum payment (making it the only relevant number) or the full balance (making the situation feel unresolvable). Neither is anchored correctly.

Operationalize it: Always show the full balance first, then the plan amount, then a per-day or per-week breakdown if helpful. A $47 monthly payment feels trivial against a $1,340 balance. It feels arbitrary when shown in isolation.

Tactic 7: Ease Framing

What it is: When required actions are framed as "easy," "quick," or "simple," people are measurably more likely to act on them. This is one of the most under-used tactics in collections — and one of the most powerful, because inaction is always the path of least resistance unless friction is made invisible.

Why it matters: The standard digital collections journey is a friction machine. Log in. Navigate. Find the payment section. Select a plan. Enter details. Submit. Each additional step is a dropout point. Symend's 2023 consumer research found that 71% of customers feel overwhelmed or anxious when receiving messages from service providers — up 47% from 2022 (Symend Decoding Billpayer Behavior Report, 2023). Ease framing — explicitly signaling how little effort is required — disarms that anxiety and removes the psychological barrier to action.

Operationalize it: Pre-fill plans wherever possible. Use opt-out framing rather than opt-in. Frame the action in plain, low-effort language ("one tap to confirm," "no login needed"). Design for one-tap resolution. Offer auto-pay enrollment as a default. Every click removed is a conversion gained — without manufacturing artificial urgency.

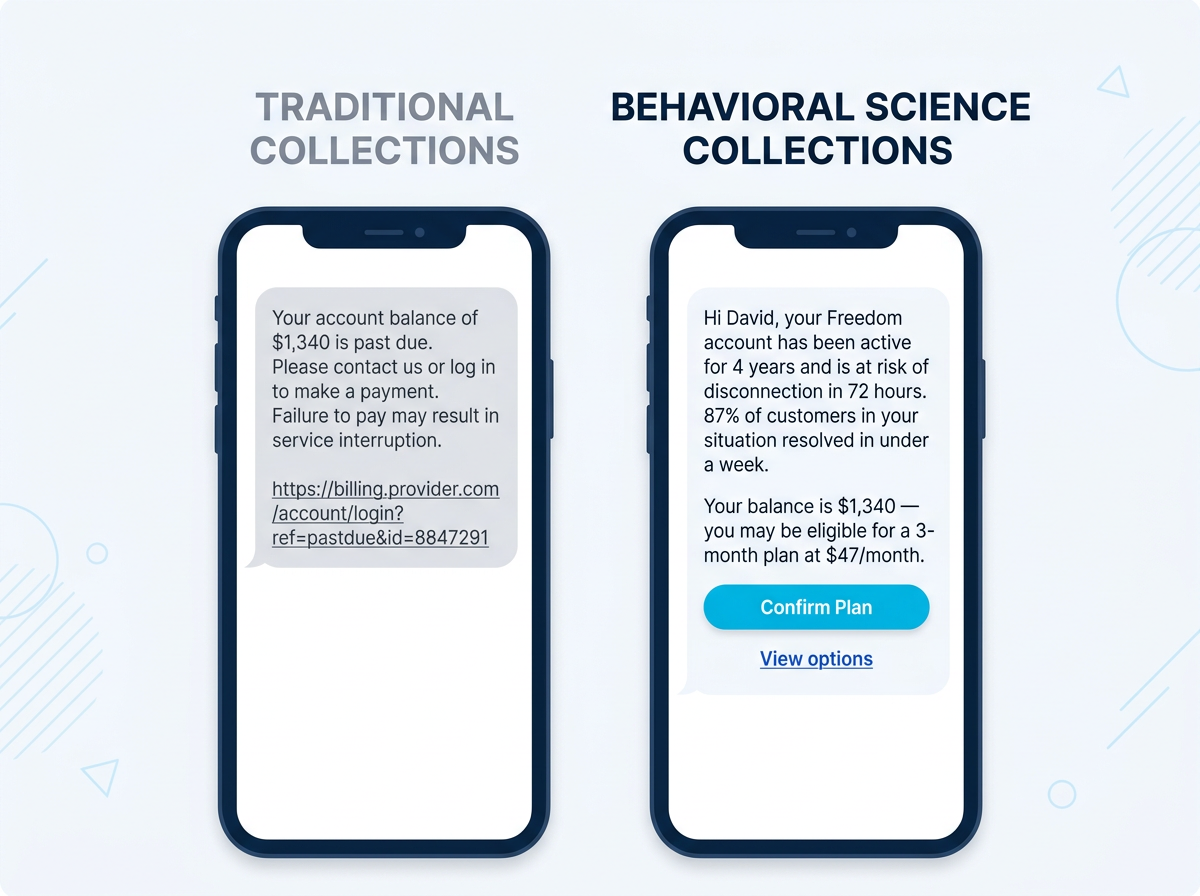

The Compound Effect: All 7 Tactics in One Message

Each tactic, applied individually, improves outcomes. Applied together, the effect compounds. Here is a single before-and-after SMS illustrating what this looks like in practice.

This message contains: a number with no anchor context, a generic CTA with unspecified friction, a vague future threat, and no social herding, endowment framing, or specificity about what the customer stands to lose.

Seven elements. All 7 tactics. Every phrase is doing psychological work.

The Science at Scale

Applying behavioral science to collections messaging isn't theoretical. A 13-million-person field experiment published in the Proceedings of the National Academy of Sciences demonstrated that behaviorally-informed email redesigns reduced 60-day delinquencies by 0.42 percentage points — and that at full scale, the best-performing intervention was estimated to have averted approximately 79,800 sixty-day delinquencies (Perez-Cavazos et al., PNAS, January 2025). The study also found that describing potential savings in percentage terms rather than dollar terms reduced delinquencies by a further 0.14 percentage points — a direct manifestation of anchoring and framing effects in practice.

This wasn't a laboratory study. It was conducted by the U.S. Department of Education on real loan borrowers, at real scale, with real financial consequences. The behavioral interventions outperformed standard communications not because the borrowers were different — but because the messages were.

Symend's own results across more than 250 million delinquency treatments tell a consistent story: behavioral science-driven engagement produces up to 10% higher recovery rates, up to 85% reduction in agent interactions, 50% reduction in OpEx costs, and 152% increases in engagement rates compared to legacy approaches — at 10x ROI for enterprise clients.

The behavioral science is not a feature of SymendCure. It is the foundation. Every engagement journey — across telecommunications, financial services, utilities, and auto financing — is built on the same principle: understand how customers actually make decisions under financial stress, and design every touchpoint around that reality.

That principle extends beyond outbound messaging. SymendConverse applies the same behavioral tactics inside conversational AI, dynamically adjusting tone and tactic based on each customer's archetype — while SymendPrevent applies them earlier in the customer lifecycle, before delinquency takes hold.

Start With a Message Audit

Every message your past-due customers receive is either working with their psychology or against it. The 7 tactics above are the predictable, consistent forces shaping whether a customer who intends to pay actually does.

Operationalizing behavioral science doesn't require a complete technology overhaul. It starts with auditing your current message library against these seven principles. Which messages lead with gains when they should lead with losses? Which present six options when two would perform better? Which require five steps when one would suffice? Which fail to signal how easy the action actually is?

The gap between a message that converts and one that doesn't is rarely about what the customer can afford. It is almost always about what the message asked of them — psychologically.

250 million delinquencies cured. The behavioral science is the reason.

Ready to see what this looks like in production?

Request a demo, explore Symend's resource library, or calculate your potential impact with the Cost Savings Calculator.

REQUEST A DEMO