Behavioral Science Isn't an Ingredient. It's the Architecture.

Why "behavioral" in collections has become a buzzword — and what separates the platforms that mean it from the ones that don't.

Key Takeaways

- "Behavioral" has become a buzzword. Nearly every collections vendor now claims it — which makes the term almost useless for telling platforms apart.

- Behavioral analytics measures what happened. Behavioral science changes what happens next. One scores and routes customers; the other diagnoses the psychological mechanism behind their delinquency and designs the intervention around it.

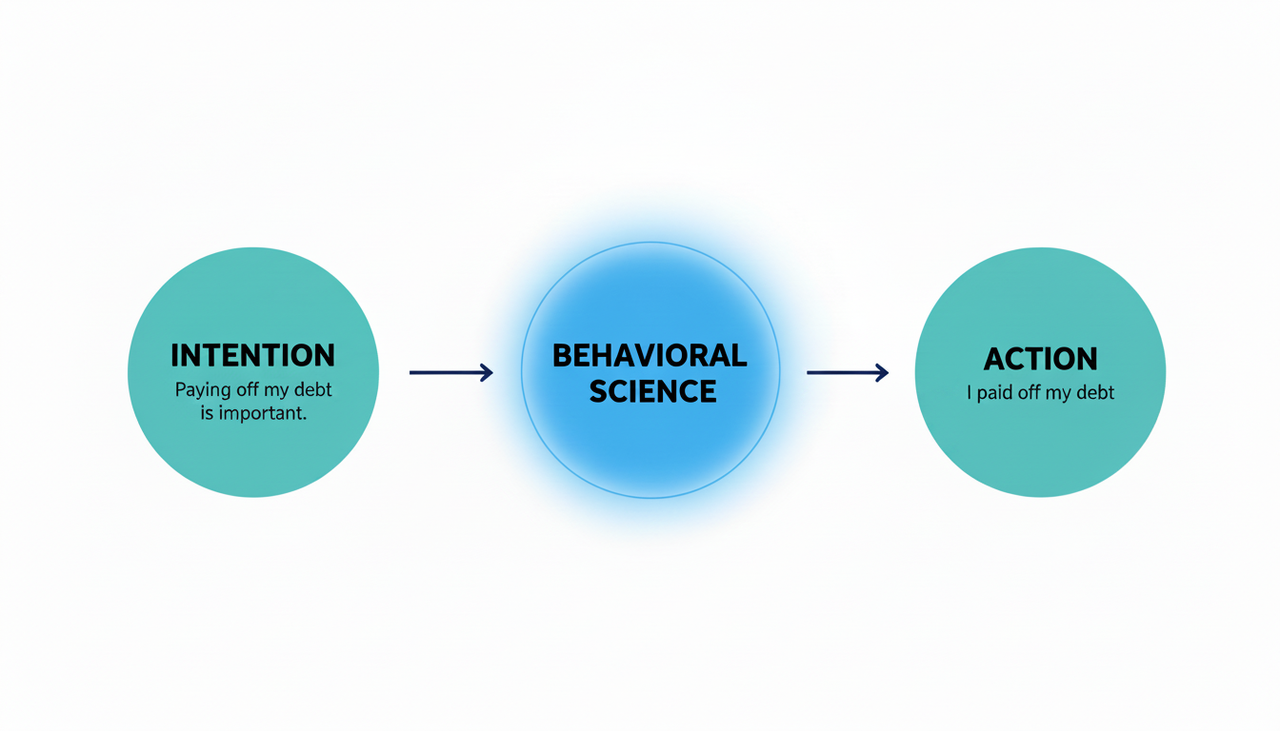

- The intention-action gap is the real problem. Most past-due customers intend to pay but don't follow through — and high-frequency pressure outreach makes that avoidance worse, not better.

- A behavioral-science-first platform changes three things: it segments on capacity and readiness, designs interventions around cognitive mechanisms, and treats empathy as a recovery strategy rather than a soft layer.

- This matters more in 2026. With delinquency at multi-decade highs across credit cards and auto loans, and AI letting you act at scale, the wrong strategy just lets you be wrong faster. SymendCure is built behavioral-science-first.

Open any enterprise collections RFP response in 2026 and you'll find a familiar word: behavioral. Behavioral scoring. Behavioral segmentation. Behavioral AI. Vendors who five years ago talked about predictive models and contact strategies have quietly rewritten their decks. The category has decided that "behavioral" sells.

That's a problem — not because behavioral science doesn't belong in collections, but because the word has been stretched until it means almost nothing. When everyone claims behavioral expertise, the term stops helping buyers tell platforms apart. And the platforms that have genuinely built around behavioral science get lumped in with the ones that have just rebranded their dashboards.

So it's worth being precise. There's a real distinction between behavioral analytics and behavioral science, and it determines whether a collections platform actually changes customer behavior — or just measures it more accurately.

Behavioral Analytics Measures What Happened. Behavioral Science Changes What Happens Next.

Behavioral analytics is the discipline of looking at observed transactions and engagement signals and using them to build scores, segments, and predictions. Did the customer open the email? Did they pay last cycle? What's their probability of curing in the next 30 days? It's useful work, and most modern collections platforms do some version of it.

Behavioral science is something different. It draws on psychology, sociology, and cognitive science to understand why people make the decisions they do — especially under financial stress, which is when most past-due customers are making them. It's interested in the gap between intention and action: the well-documented fact that wanting to pay a bill and actually paying it are governed by different mental processes, and that the second process can be influenced by how, when, and through what channel you communicate.

"Behavioral analytics tells you which customer is likely to pay. Behavioral science tells you what to do about it."

The difference shows up in the design of the system. A platform built on behavioral analytics scores customers and routes them. A platform built on behavioral science scores customers, understands the psychological mechanism behind their delinquency, and designs the intervention to counter or leverage that mechanism. One is a sorting hat. The other is a strategy.

The Intention-Action Gap Is the Problem Collections Has Been Quietly Ignoring

Most past-due customers aren't refusing to pay. Research and operator data both show that the majority intend to resolve their balance. Something gets in the way: stress narrows their focus, decision fatigue makes them avoid the inbox entirely, shame leads to ostrich-effect avoidance, or the message they received didn't match what they actually needed to act.

Behavioral science is the bridge between a customer's intention to pay and the action of actually paying.

This is the intention-action gap, and it's the central problem behavioral science was developed to address. In a clinical setting it's why patients don't take prescribed medication. In a public-health setting it's why people don't show up to vaccination appointments they signed up for. In collections, it's why a customer who told you on Tuesday that they'd pay on Friday hasn't paid by the following Wednesday.

Generic outreach — the kind that legacy platforms automate at scale — assumes the gap doesn't exist. It assumes that if you just send enough reminders, customers will act. The data has been making it clear for years that this isn't true. Consumers now receive hundreds of digital messages a day. Pressure-based, high-frequency outreach hits diminishing returns fast, and often backfires by deepening the avoidance behavior it was meant to break.

"Past-due customers aren't ignoring you because they don't care. They're ignoring you because their brain is doing exactly what brains do under financial stress."

What "Behavioral Science First" Actually Looks Like in Practice

If a platform is built on behavioral science rather than on top of it, three things change about how it operates.

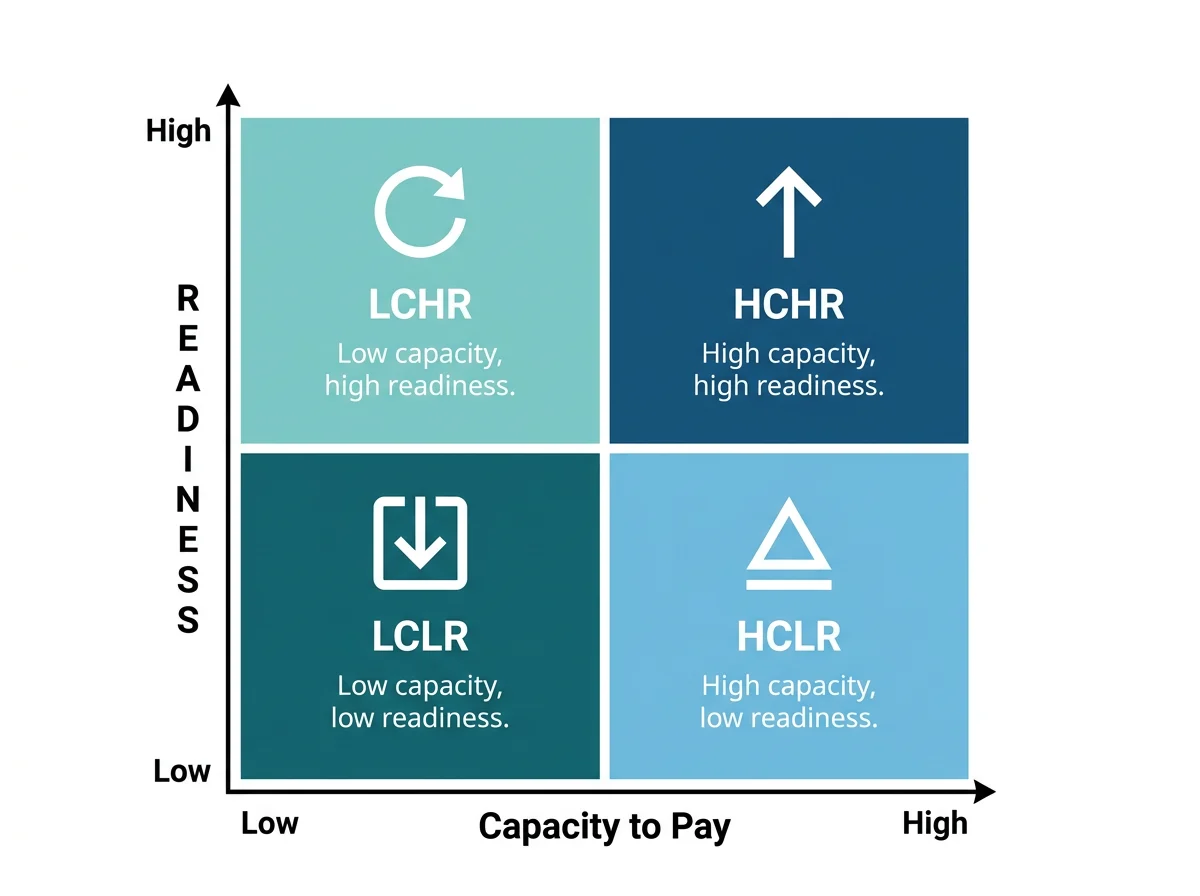

1. Segmentation is built on capacity AND readiness, not just risk

Traditional risk-based segmentation puts customers into high, medium, or low buckets based on the likelihood they'll pay. It's a single dimension, and it conflates two very different psychological states: customers who can pay but aren't ready to engage, and customers who are ready to engage but can't pay. Those customers need opposite interventions. A risk score can't tell them apart.

A behavioral-science-first platform segments on at least two axes — capacity to pay and readiness to act — producing archetypes that reflect distinct decision-making patterns. A customer with high capacity and low readiness (the kind who pays right before consequences hit) needs a different message than a customer with low capacity and high readiness (the kind who wants to resolve the debt but is financially constrained). Same risk band; entirely different playbook.

Symend's Delinquency Archetypes segment past-due customers by capacity to pay and readiness to act — not just a single risk score.

2. The intervention is designed around a psychological mechanism, not a message template

Behavioral analytics tells you to send a customer an email. Behavioral science tells you which cognitive bias that email needs to counter. A customer in a state of tunneling under financial scarcity needs the message simplified, the next step made trivially actionable, and the cognitive load reduced. A customer exhibiting decision-from-experience bias — the one who has paid late before with no real consequence — needs the framing of risk to change. These aren't message-template choices. They're intervention-design choices.

This is the level at which behavioral-science-first platforms operate: not just on which channel to use or which day to send, but on which specific behavioral mechanism a piece of communication needs to address. The tone, the framing, the choice architecture inside the message — all of it gets tuned to the psychology of the recipient, not just their balance and tenure. (For a concrete breakdown, see the seven behavioral tactics that determine whether a customer pays or ignores you.)

3. Empathy isn't a soft layer — it's a recovery strategy

There's a tendency in enterprise software to treat empathy as the polite version of customer experience: nice to have, hard to measure, easy to cut when targets are tight. Behavioral science argues the opposite. Empathy isn't softening the message; it's matching the message to the actual cognitive state of the customer receiving it. That's why empathetic, archetype-aligned outreach consistently outperforms high-frequency pressure campaigns on the metrics that operators actually care about — cure rates, roll rates, and downstream retention.

Symend client deployments and the broader research base both show the pattern: when past-due engagement is redesigned around behavioral science, outbound volume can drop substantially while cure rates rise. The lesson isn't "send less." It's that pressure is a blunt instrument and the right intervention, delivered the right way, does more work with less noise.

Why This Matters More in 2026 Than It Did Five Years Ago

Two trends have made the behavioral-science-vs-analytics distinction sharper. The first is the volume of digital communication consumers are now wading through — hundreds of messages a day, by most measures. The second is the rise of AI-powered collections tools that can generate, personalize, and dispatch outreach at a scale that would have been unimaginable a decade ago.

Both trends amplify the same risk: if your platform doesn't understand why customers behave the way they do, AI just lets you be wrong faster. More personalized messages aren't automatically better messages. More frequent contact isn't automatically more recovery. The capability to act at scale only translates into outcomes when it's pointed at the right psychological lever.

And the stakes have rarely been higher. Across every major consumer-credit category, delinquency is climbing to levels not seen in years — which means the cost of running the wrong collections strategy is climbing with it. The economic climate has made getting this right more urgent, not less:

The pattern across these markets is the same one behavioral science predicts: today's delinquency is driven far more by capacity and psychology than by forgetfulness. Customers caught in an affordability squeeze don't need another reminder — they need the right intervention, matched to their actual situation. That's exactly the gap between a platform that measures behavior and one that's engineered to change it.

This is the argument for putting behavioral science at the foundation of a collections platform rather than treating it as a feature inside one. AI is the engine. Behavioral science is the steering.

How to Tell Whether a Platform Actually Leads With Behavioral Science

Three questions tend to separate the two camps quickly:

- Ask how the platform segments customers beyond risk score. If the answer is "more granular risk tiers," it's behavioral analytics. If the answer involves distinct psychological profiles tied to capacity and readiness, it's closer to behavioral science.

- Ask how the platform decides what message to send to a given segment. If the answer is "we test variants and keep what works," it's analytics-driven optimization. If the answer involves identifying the cognitive mechanism driving the behavior and designing the intervention to address it, it's behavioral-science-driven.

- Ask where the behavioral science team sits in the company. If there isn't one — if behavioral expertise lives in marketing copy rather than in product and data science — the foundation isn't really there.

None of this is a knock on analytics. Collections operations need both. But the order matters. Analytics layered onto a behavioral science foundation produces interventions that get smarter over time. Behavioral language layered onto an analytics-only foundation produces marketing.

The Bottom Line

The vendors that win the next decade of enterprise collections won't be the ones with the loudest AI claims. They'll be the ones that have built their platforms around a genuine understanding of how past-due customers make decisions — and have engineered every layer above that foundation, from segmentation to message design to optimization, to act on that understanding.

If you want to see what a behavioral-science-first platform looks like in practice, the Delinquency Archetype framework behind SymendCure is the place we'd start. For a deeper read on how this approach applies to your industry, see how it plays out in telecommunications collections, financial services, and utilities.

See behavioral science built into the architecture

Explore collections engagement designed around how past-due customers actually make decisions — not bolted on as a feature. Book a 15-minute demo.

EXPLORE SYMENDCURE REQUEST A DEMO