The Five-Layer Architecture Banks Are Using to Combat Rising Delinquencies

As delinquency rates surge to post-pandemic highs, the solution isn't more technology—it's the right architecture connecting data, intelligence, engagement, orchestration, and measurement.

Key Takeaways

- U.S. household debt hit $18 trillion with 3.6% delinquent; Canadian consumer debt reached $2.56 trillion with Ontario mortgage delinquencies surging 90% YoY

- Fragmented infrastructure creates hidden costs—leading banks are consolidating into unified five-layer architecture

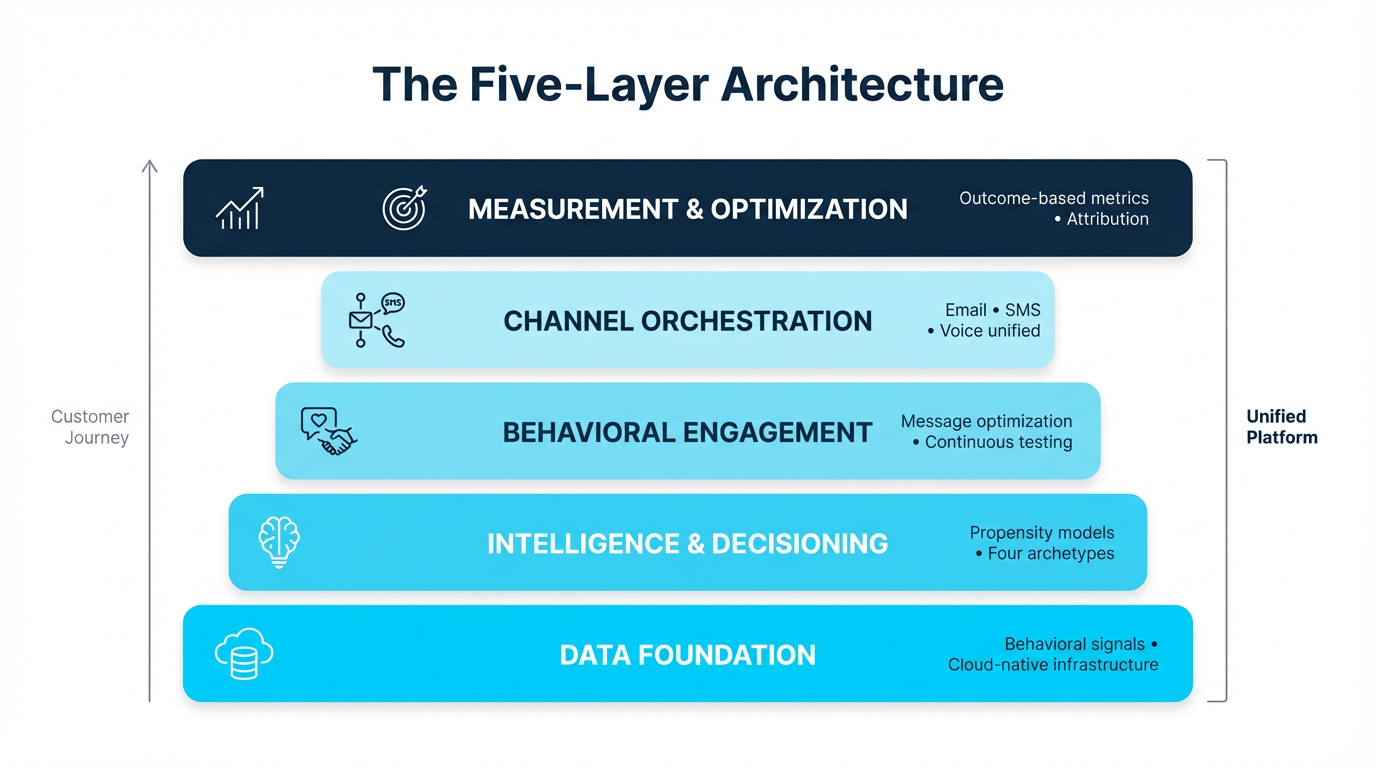

- The five layers: Data Foundation, Intelligence & Decisioning, Behavioral Engagement, Channel Orchestration, and Measurement & Optimization

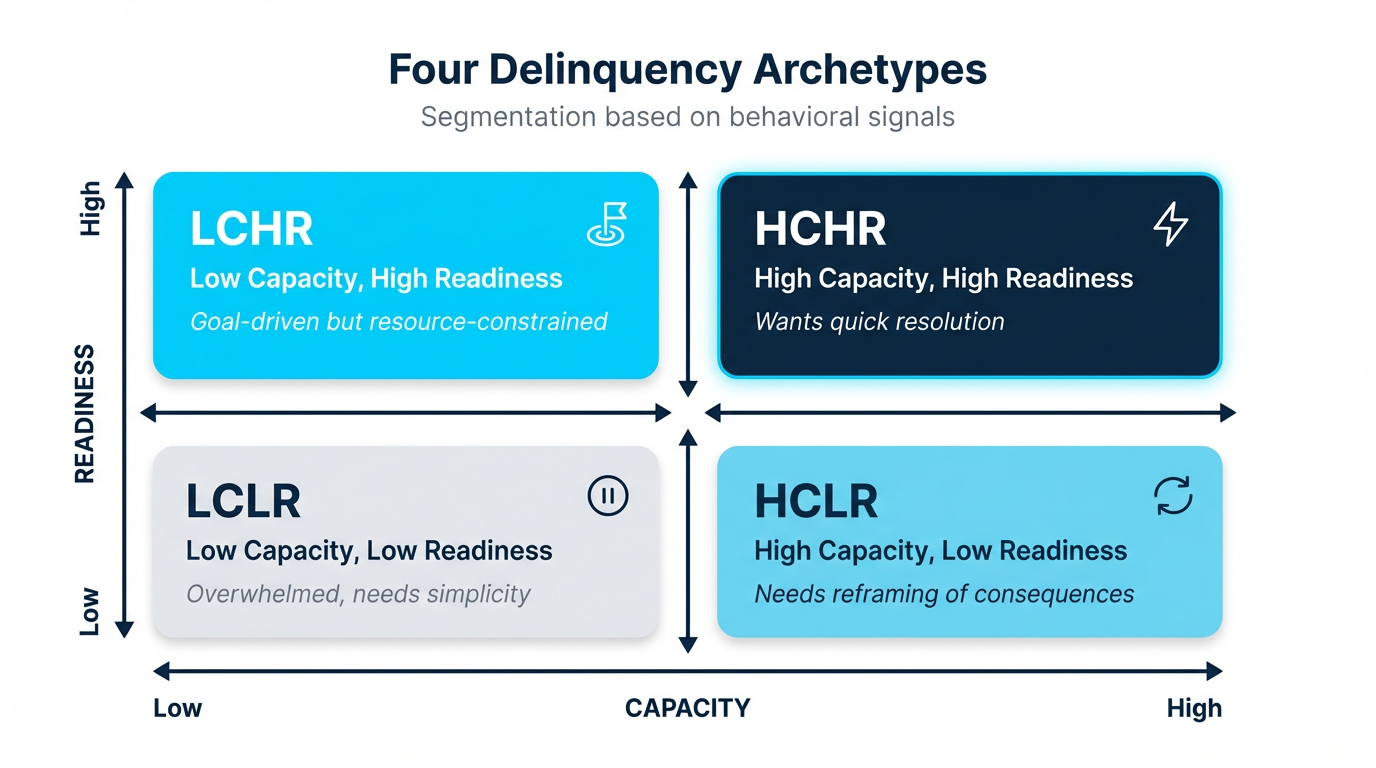

- Four Delinquency Archetypes (HCHR, HCLR, LCHR, LCLR) reveal why customers aren't paying, enabling targeted engagement

- Organizations don't need to rip and replace—behavioral engagement works as a complementary layer requiring just 12 data fields to start

The numbers are stark. U.S. household debt hit $18 trillion by the end of 2024, with 3.6% of all debt delinquent (Federal Reserve Bank of New York, Household Debt and Credit Report Q4 2024). In Canada, total consumer debt reached $2.56 trillion (up 4.6% year-over-year), with Ontario mortgage delinquencies surging 90% year-over-year (Equifax Canada, Market Pulse Q4 2024).

Among the poorest 10% of U.S. ZIP codes, the share of people with delinquent credit card debt jumped from approximately 11% in mid-2021 to 17.4% by early 2024 (St. Louis Fed, On the Economy Blog).

Collections teams face larger volumes of at-risk accounts while operating with constrained budgets. The projected financial outlook demands cost-effective solutions that maintain strong performance.

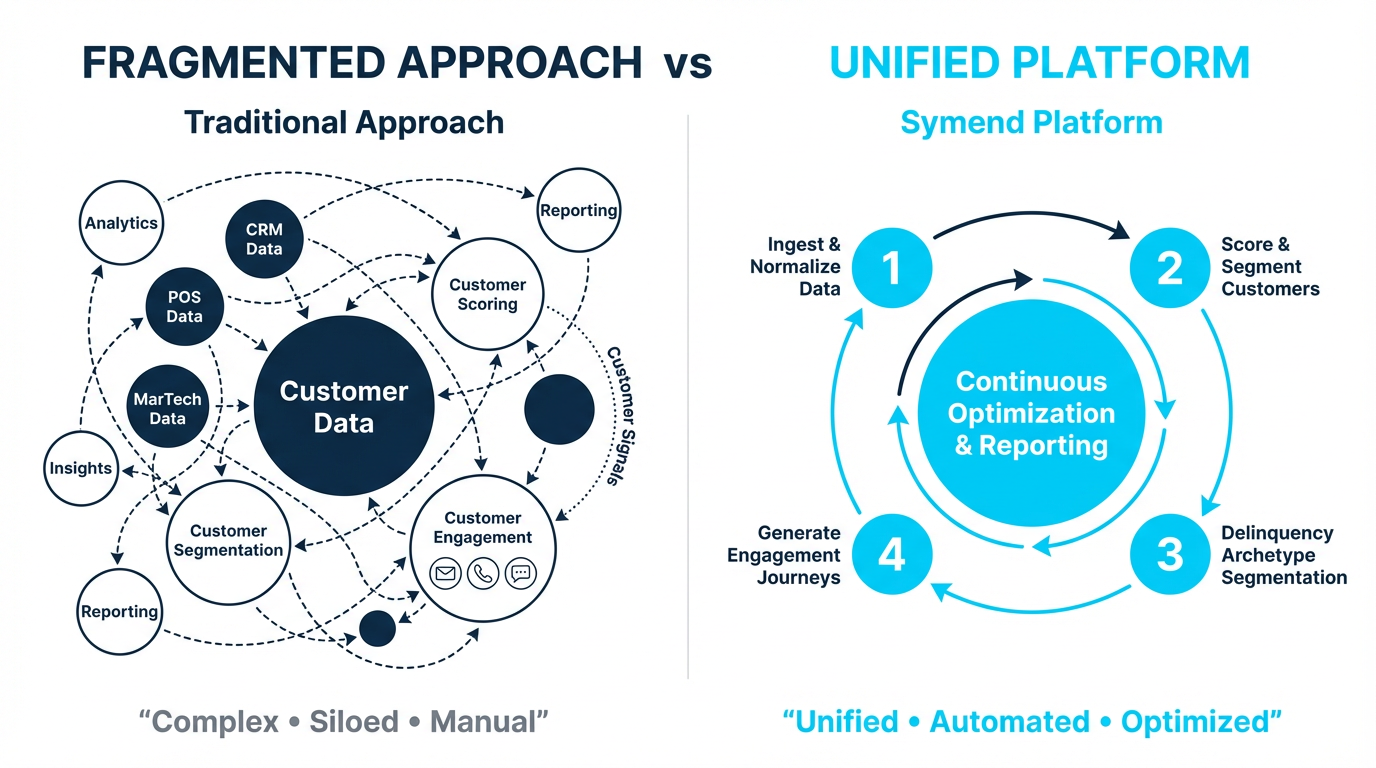

Yet many organizations respond to this challenge by adding more tools—another decisioning engine, another communication platform, another analytics dashboard. The result: fragmented infrastructure that creates its own costs.

Banks with fragmented engagement infrastructure report significantly higher cost-to-collect and lower customer satisfaction scores.

The Unified Architecture Approach

Leading financial institutions are taking a different path: consolidating customer engagement capabilities into a unified architecture that enables what fragmented solutions cannot—learning from customer behavior across all touchpoints to continuously improve engagement effectiveness.

Layer 1: Data Foundation

The foundation isn't about collecting more data. It's about creating decision-grade behavioral signals from the data you already have.

Engagement patterns, channel preferences, friction points, prior response—these signals inform personalized tone, timing, and treatment. Traditional collections systems rely on batch cycles. Modern engagement architecture supports in-cycle learning: testing and adapting based on customer response in days, not quarters.

Layer 2: Intelligence & Decisioning

Risk scores predict probability of default. They don't predict what communication approach will motivate payment.

The intelligence layer adds behavioral propensity models that segment customers by capacity to pay and readiness to act. This creates psychological archetypes rather than just credit score tiers.

Four archetypes matter:

High Capacity, High Readiness (HCHR): Customers who can pay and want to resolve quickly. Driven by uncertainty avoidance.

High Capacity, Low Readiness (HCLR): Customers who can pay but aren't motivated. May exhibit decision-making gaps.

Low Capacity, High Readiness (LCHR): Customers who want to pay but face genuine financial constraints. Motivated by goals.

Low Capacity, Low Readiness (LCLR): Customers facing overwhelming financial stress. Interventions must reduce cognitive bandwidth demands.

Layer 3: Behavioral Engagement

This layer converts intelligence into action. Key principles include Prospect Theory, Present Bias, Social Proof, and Cognitive Load Reduction—applied through continuous multi-armed bandit optimization, not quarterly A/B tests.

Layer 4: Channel Orchestration

Unified channel orchestration ensures consistency across email, SMS, voice, and digital. This layer manages frequency caps, compliance controls, and escalation logic across jurisdictions.

Layer 5: Measurement & Optimization

The measurement layer tracks outcome-based metrics: actual payment behavior, cure rates by cohort, customer retention impact, and true cost-to-collect.

The Bidirectional Data Flow

Behavioral intelligence flows back to enrich enterprise data—payment propensity scores, engagement archetypes, channel preferences become queryable across Risk Management, Product Teams, Customer Experience, and Finance.

Regulatory Alignment

United States: CFPB Regulation F governs debt collector communications.

United Kingdom: FCA Consumer Duty (PS22/9) requires firms to deliver good outcomes. PS24/2 strengthened borrower protections.

Canada: PIPEDA governs personal information use. Quebec's Law 25 adds additional privacy requirements.

The Implementation Reality

Organizations don't need to rip and replace. Existing decisioning platforms continue serving their functions. Integration requirements are modest: typically 12 data fields to begin.

SymendCure works with existing enterprise platforms through standard REST APIs and secure file exchange—functioning as a complementary behavioral engagement layer rather than a replacement for existing infrastructure.

The Path Forward

Rising delinquencies aren't a technology problem with a technology solution. They're a customer engagement challenge that requires behavioral methodology at scale.

The key insight: behavioral science is the lens; AI is the horsepower that makes the methodology practical at enterprise scale.

Ready to unify your collections architecture?

Symend's behavioral science-driven platform provides comprehensive coverage across all five architectural layers, delivered as a managed service.

REQUEST A DEMOFrequently Asked Questions

Symend's AI-driven platform delivers up to 10% higher recovery rates by identifying at-risk customers early and engaging them with hyper-personalized messaging before delinquencies escalate. Using Delinquency Archetypes and behavioral science, Symend's AI predicts customer behavior and generates optimized engagement flows that drive repayment action. With 9+ years treating 250+ million delinquencies and $50B+ in recoveries, SymendCure transforms collections from reactive pursuit to proactive engagement.

Data Foundation (behavioral signals from existing data), Intelligence & Decisioning (archetype classification), Behavioral Engagement (message-level optimization), Channel Orchestration (unified multi-channel management), and Measurement & Optimization (outcome-based metrics with attribution).

Fragmented infrastructure creates hidden costs: integration complexity, data silos, and critically, reduced learning velocity. Unified architecture enables cross-channel learning that's architecturally impossible with siloed vendor solutions.

Behavioral intelligence generated during collections—propensity scores, archetypes, channel preferences—flows back to enrich enterprise data systems, making the engagement platform a behavioral intelligence generator for the entire enterprise.

They add behavioral dimensions—capacity to pay and readiness to act—creating four profiles (HCHR, HCLR, LCHR, LCLR) that reveal why customers aren't paying, each requiring fundamentally different engagement approaches.

Typically 12 data fields to begin, with incremental enrichment over time. Works with existing enterprise platforms through standard REST APIs and secure file exchange.