Why Your Past-Due Customers Aren't Paying

How to break through the barriers to repayment using behavioral science.

Most past-due customers genuinely intend to pay their bills. So why don't they? The answer lies in a fundamental truth that traditional collections strategies overlook: decision-making in debt is completely different from decision-making in abundance.

Financial stress makes it harder to think clearly. When customers are facing debt, they often choose the wrong action—or don't take any action at all. Understanding the psychology behind this paralysis is the key to breaking through and driving repayment.

Debt Is More Common Than You Think

Before we explore the psychology, let's acknowledge an important reality: debt is normal. Being past-due isn't a character flaw—it's an experience that spans all demographics and credit types.

In the US (Federal Reserve Bank of New York, Q3 2025):

- Total household debt reached a record $18.59 trillion

- 4.5% of outstanding debt is in some stage of delinquency

- 4.7% of consumers have a third-party collection account on their credit report

- Credit card and auto loan delinquency rates have risen to levels not seen since the Great Financial Crisis

In Canada (Equifax Canada, Q3 2025):

- 1.45 million consumers missed a credit payment—up 46,000 from the previous quarter

- The national 90+ day non-mortgage delinquency rate reached 1.63%, up 14% year-over-year

- Total consumer debt climbed to $2.62 trillion

- 1 in 20 consumers aged 18-35 missed a payment, with delinquencies reaching levels not seen since 2009

When we normalize debt by treating past-due customers with empathy rather than confrontation, they become more receptive to communication—and more likely to take action.

The Intention-Action Gap: Why Good Intentions Don't Lead to Payment

Here's the core problem: most customers intend to pay but either avoid taking action entirely or take actions that don't result in repayment.

Consider these scenarios:

Darryl had an expensive car repair two months ago, and now his bills are piling up. He knows he needs to address them, but he's so overwhelmed that he does nothing at all. Late fees accumulate, collection notices arrive, and his credit score plummets.

Cecilia is struggling to make her mortgage payment after being laid off. She's a couple hundred dollars short, so she goes to the casino hoping to win big. Instead, she loses what little she had.

Both customers intended to resolve their debt. Neither took effective action. This is the intention-action gap—and mental shortcuts are what cause it.

Mental Shortcuts: The Hidden Barrier to Repayment

Humans make thousands of decisions daily. To avoid cognitive overload, we rely on mental shortcuts—subconscious rules that help us navigate routine choices quickly. These shortcuts are usually helpful, but under financial stress, they often lead to poor decisions.

Three factors push past-due customers into "survival mode" where mental shortcuts take over:

- Financial stress creates a sense of scarcity that narrows focus to immediate problems rather than long-term solutions.

- Time pressure from looming deadlines reduces the ability to calmly evaluate options, leading to impulsive decisions or complete inaction.

- Negative emotional associations with debt—shame, judgment, failure—heighten anxiety and fuel avoidance.

Four Mental Shortcuts That Block Repayment

1. Cognitive Dissonance

Ruben, a recent graduate juggling student loans and medical bills, receives a payment reminder at work with an option to request an extension. He wants to take it—but doesn't click because he's worried a coworker might see. Later, his girlfriend visits, and he hides his phone again.

Ruben doesn't see himself as someone with debt problems. The gap between his self-perception and reality prevents him from taking action, even when help is offered.

2. Avoidance

Dee, a divorced mom, falls behind on her internet bill. She plans to call and arrange a partial payment, but dreads the conversation. Hockey practice, dance class, homework help—there's always a reason to put it off. Soon, she receives a disconnection notice.

Dee delays action because avoiding the problem provides temporary relief from stress—even though it makes her situation worse.

3. Prospect Theory

Janey takes out a payday loan to cover her bills, focusing on the immediate relief of meeting her obligations. She doesn't fully consider the 730% APR that will make repayment far more difficult.

The desire to resolve immediate pain overrides consideration of long-term consequences.

4. Optimism Bias

Josh carries a $6,500 credit card balance but keeps telling himself he'll pay it off when he gets a raise. He's been expecting that raise for two years. Meanwhile, the 24.62% interest keeps compounding.

Unrealistic optimism about future circumstances delays present action.

Counteracting Mental Shortcuts

Mental shortcuts like cognitive dissonance, avoidance, prospect theory, and optimism bias heavily influence how customers react to collections messages. When we recognize which shortcuts are at play, we can adapt our messaging to reframe their situations in a more positive, empowering, and action-inducing light.

Let's look at how to counteract the four mental shortcuts we identified above:

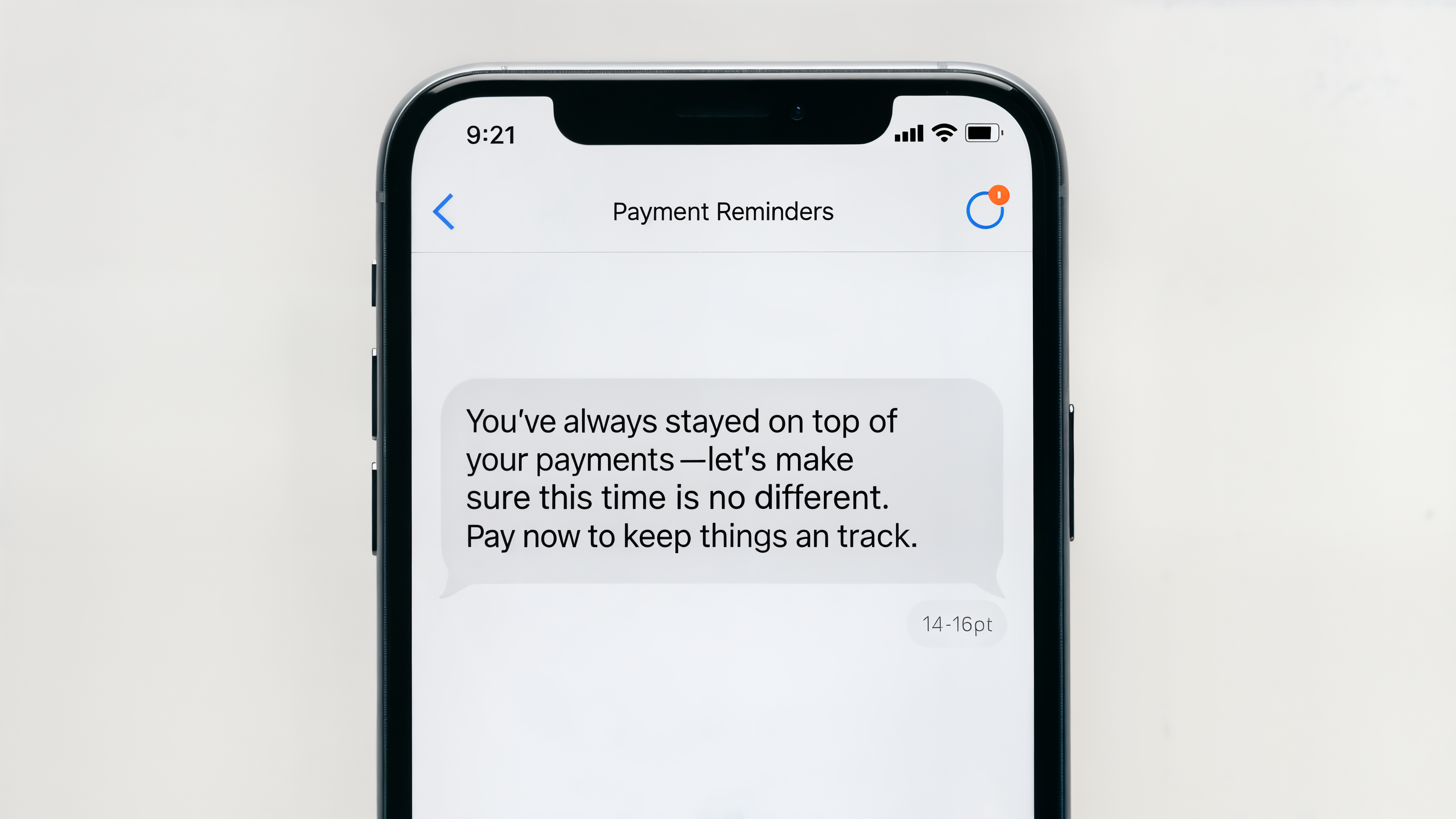

For cognitive dissonance: Align messaging with the customer's self-image as a responsible person. "You've always stayed on top of your payments—let's make sure this time is no different. Pay now to keep things on track."

For avoidance: Reduce friction and eliminate the need for dreaded conversations. Offer self-service options and emphasize how easy the process is. "No phone calls needed—resolve your balance in just a few clicks."

For prospect theory: Help customers see the long-term consequences of short-term relief. "A small payment today prevents bigger costs tomorrow. Avoid late fees and protect your credit score."

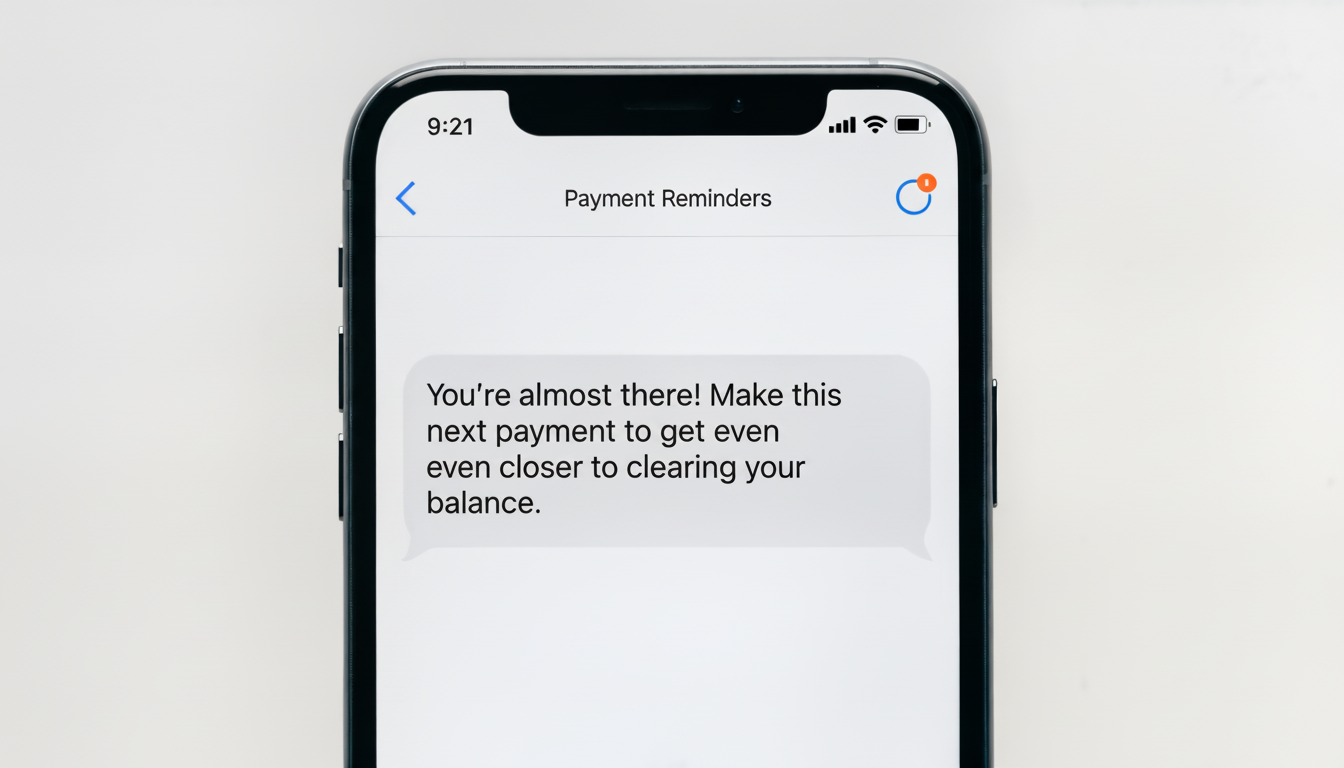

For optimism bias: Ground customers in their current reality while still offering hope. "Your balance is $287.36 today. Take action now to prevent it from growing—set up a payment plan that fits your budget."

Leveraging Mental Shortcuts for Positive Action

We can also use mental shortcuts in favor of repayment by crafting messages that align with how customers naturally think.

Reciprocity principle: When treated with kindness, people respond in kind. "You're a valued customer, and we don't want to say goodbye. Let's work through this together."

Implementation intentions: People follow through when given clear "if-then" plans. "Take the first step by making a payment now. Next, consider signing up for a payment plan."

Urgency heuristic: Clear deadlines motivate action. "Pay your balance within the next 24 hours to avoid suspension of service."

Fresh start effect: New beginnings inspire change. "Let's start the month fresh by setting up autopay for your bill!"

The Results Speak for Themselves

When behavioral science principles are applied to collections strategy, the outcomes are dramatic:

A Better Approach for Everyone

Traditional collections treats past-due customers as adversaries. But antagonizing customers isn't good for business—it erodes trust, damages relationships, and often fails to recover payment.

Applied behavioral science offers a different path. By understanding the psychological factors that prevent repayment, we can craft outreach that resonates with customers and inspires positive action. This improves cure rates while enhancing customer satisfaction and strengthening long-term relationships.

The result is sustainable recovery that works for both the business and the customer.

Free eBook

Why Your Past-Due Customers Aren't Paying

Discover the psychological barriers to payment and proven behavioral science strategies that achieve 80% reduction in outbound calls while boosting cure rates.

DOWNLOAD THE EBOOKFrequently Asked Questions

Applied behavioral science is the study of how people make decisions under various circumstances—and how we can ethically influence those decisions to improve outcomes. In collections, it explores how stress, emotions, and financial pressure affect a customer's response to outreach, then uses those insights to create more effective, empathetic communication strategies.

The intention-action gap occurs when mental shortcuts—cognitive biases and heuristics—interfere with follow-through. Under financial stress, customers often fall into survival mode where their focus narrows to immediate relief rather than long-term solutions. This can lead to avoidance, impulsive decisions, or complete inaction, even when they genuinely want to resolve their debt.

Symend's platform is purpose-built for debt recovery, with behavioral science principles integrated into every aspect of segmentation and messaging. Unlike generic AI tools that generate polished but psychologically uninformed messages, Symend analyzes where each customer is in their debt journey and applies specific behavioral tactics—like reciprocity, implementation intentions, or the fresh start effect—to guide them toward positive action.

Symend is a next-gen engagement platform transforming enterprise collections with the power of AI and Behavioral Science. Symend predicts a customer's behavior based on Delinquency Archetypes and generates AI-optimized, hyper-personalized engagement journeys that break through the noise. With over 9 years of experience treating over 250 million delinquencies and over $50 billion in recoveries, Symend delivers up to 10% higher recovery rates, 50% reduction in OpEx costs and 10x ROI while strengthening customer relationships for enterprise telecommunications, financial services, and utilities companies.

Symend delivers 10x ROI through multiple value streams: up to 10% higher recovery rates, 85% reduction in agent interactions and call volume reduces OpEx costs by 50%, decreased text/email/letter costs, improved write-off rates, and reduced third-party fees. With over $50 billion in proven recoveries across over 250 million delinquencies, Symend clients see millions in additional recovered revenue while strengthening customer relationships.

Want to learn how behavioral science can transform your debt recovery strategy? Book a demo to discover a better approach.