AI Debt Collection Software: How It Works and What to Look For

Predictive analytics, behavioral science, and machine learning are transforming how organizations recover debt while preserving customer relationships

Key Takeaways

- AI debt collection software uses predictive models to determine the right message, channel, and timing for each customer

- Organizations using behavioral science-powered AI platforms report up to 10% higher recovery rates and significantly improved customer outcomes

- The shift from rules-based automation to agentic AI represents the third generation of collections technology

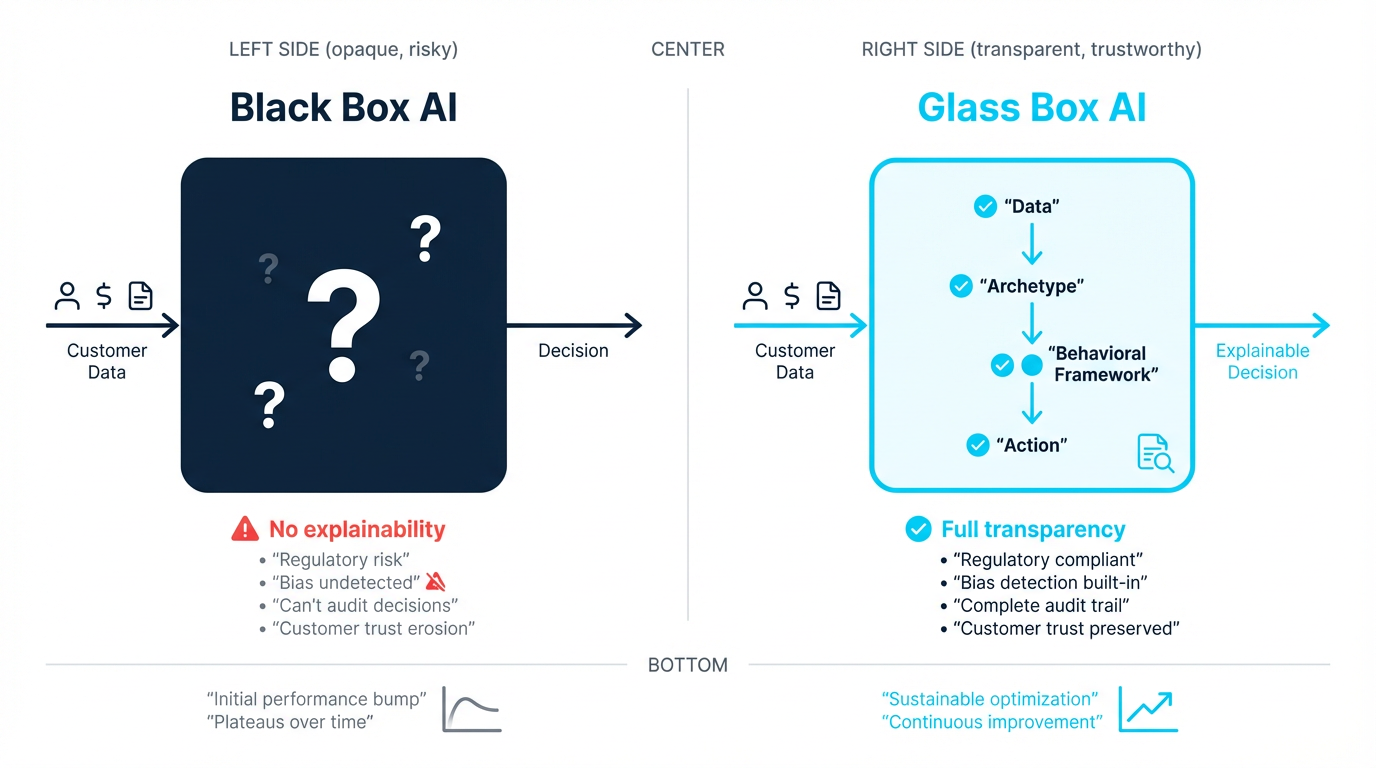

- Not all AI is equal: glass box (explainable) AI outperforms black box approaches on compliance, trust, and long-term results

- Behavioral science-driven segmentation by capacity and readiness to pay delivers better outcomes than risk scoring alone

What Is AI Debt Collection Software?

AI debt collection software is a technology platform that uses artificial intelligence, machine learning, and predictive analytics to automate and optimize the recovery of outstanding debts. Unlike rules-based automation that follows static "if/then" logic, AI-powered platforms analyze thousands of data points per customer to dynamically determine the best engagement strategy.

The core difference: traditional collection software tells you who to contact and when. AI-powered platforms that combine behavioral science also answer how to motivate each customer to act — by understanding their individual circumstances, psychological barriers, and readiness to engage.

AI collections software vs. debt management software: Debt collection software focuses on recovering delinquent accounts through outreach and payment arrangements. Debt management software is a broader category that includes portfolio tracking and pre-delinquency monitoring. The most advanced platforms combine both, offering early intervention alongside active recovery. Read our complete buyer's guide for a full comparison.

How AI Improves Debt Recovery

AI transforms collections by making every customer interaction more relevant, better timed, and delivered through the right channel. Here's how the core capabilities work together:

Predictive Customer Segmentation

Most AI platforms segment customers by risk score, demographics, and payment history — an improvement over static rules, but still limited. The most advanced platforms go further by incorporating behavioral science, segmenting based on capacity to pay and readiness to engage. This dual-axis approach enables personalized strategies that pure risk scoring cannot match.

Optimal Timing and Channel Selection

AI models analyze engagement history to predict when each customer is most likely to open a message, read it, and act. The platform automatically selects the best channel, whether SMS, email, voice, or web portal, and the optimal time to reach out, down to the hour.

Empathetic, Personalized Messaging

Generic AI platforms personalize the name and balance but use the same tone and framing for every customer. Platforms that layer behavioral science on top of AI go further — they adapt tone, framing, and call-to-action based on what motivates each customer. A customer experiencing temporary financial hardship needs a fundamentally different message than one who simply forgot. Only a behavioral approach identifies these differences and tailors engagement accordingly.

Continuous Learning and Optimization

Every interaction generates data. AI platforms use this feedback loop to continuously refine their models, running automated experiments across messaging, timing, and channel strategies. What works gets amplified; what doesn't gets eliminated. This is the key advantage over static rules: the system gets smarter with every customer interaction.

Key AI Capabilities to Evaluate

Not all "AI-powered" platforms are created equal. When evaluating AI debt collection software, look for these specific capabilities:

| Capability | What to Look For | Why It Matters |

|---|---|---|

| Behavioral Segmentation | Segments by capacity + readiness to pay, not just risk score | Personalized strategies per customer archetype |

| Predictive Analytics | Predicts payment likelihood, optimal timing, best channel | Higher contact rates and conversion |

| Next-Best-Action Engine | Recommends specific actions based on real-time customer data | Agents and automation act on intelligence, not guesswork |

| Multi-Channel Orchestration | AI-driven channel selection across SMS, email, voice, portal | Reaches customers where they engage |

| Conversational AI | Natural language interactions that de-escalate and guide to resolution | Handles routine interactions, freeing agents for complex cases |

| Automated Experimentation | Continuous A/B testing of messages, timing, and strategies | Compounding performance improvement over time |

| Explainable AI (Glass Box) | Every decision is traceable and auditable | Regulatory compliance, bias prevention, stakeholder trust |

| Compliance Automation | Built-in FDCPA, TCPA, CFPB, and jurisdiction-specific rules | Reduces violation risk as regulations evolve |

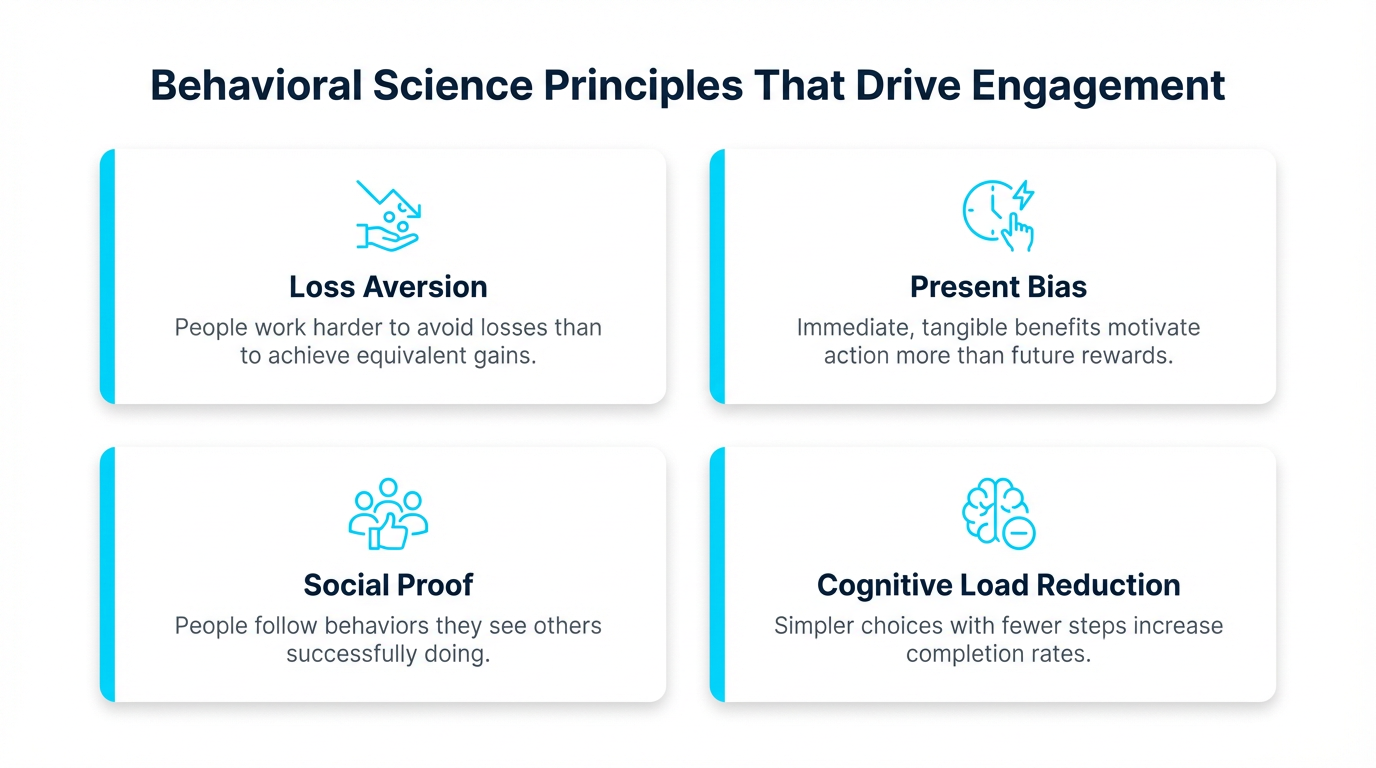

Why AI Alone Isn't Enough: The Behavioral Science Difference

Many vendors now claim "AI-powered" collections. But AI is a tool, not a strategy. The real question isn't whether a platform uses AI; it's what the AI is optimizing for and what science governs the decisions.

There are three tiers of collections technology, and the differences in outcomes are significant:

| Dimension | Traditional Collections | Generic AI Platforms | Behavioral Science + AI |

|---|---|---|---|

| Approach | Agent calls, generic letters | Automated outreach, basic personalization | Engagement strategies driven by customer psychology |

| Recovery Improvement | Baseline | Initial bump, then plateau | Up to 10% sustained increase that compounds over time |

| Customer Segmentation | Balance and days past due | Risk score and demographics | Behavioral archetypes: capacity + readiness to pay |

| Customer Experience | Aggressive, damages relationships | Less aggressive, still impersonal | Empathetic, preserves customer lifetime value |

| Optimization | Quarterly manual review | Model retraining on schedule | Continuous experimentation across messaging, timing, channel |

| Compliance | Manual monitoring | Basic automated rules | Glass box explainability with full audit trails |

| Long-term Trajectory | Declining returns | Flat after initial gains | Compounding improvement as models learn |

The "initial bump" trap: Generic AI tools applied to collections often produce quick early gains that plateau within months. This happens because they optimize for contact efficiency — reaching more people faster — without understanding why customers aren't paying. Platforms grounded in behavioral science address the root causes of non-payment, which is why their improvements compound rather than plateau. Read why generic AI may be driving customers away.

The Power of Behavioral Design: A Proof Point

The impact of behavioral design on collections outcomes can be dramatic. In one documented experiment, simplifying a payment page from seven options to two focused calls-to-action produced a 675% increase in positive customer sentiment and a 133% lift in payment likelihood — a direct demonstration of how choice architecture shapes customer behavior. It's not the volume of options that drives action; it's how clearly the right option is presented.

See the full choice architecture case study →

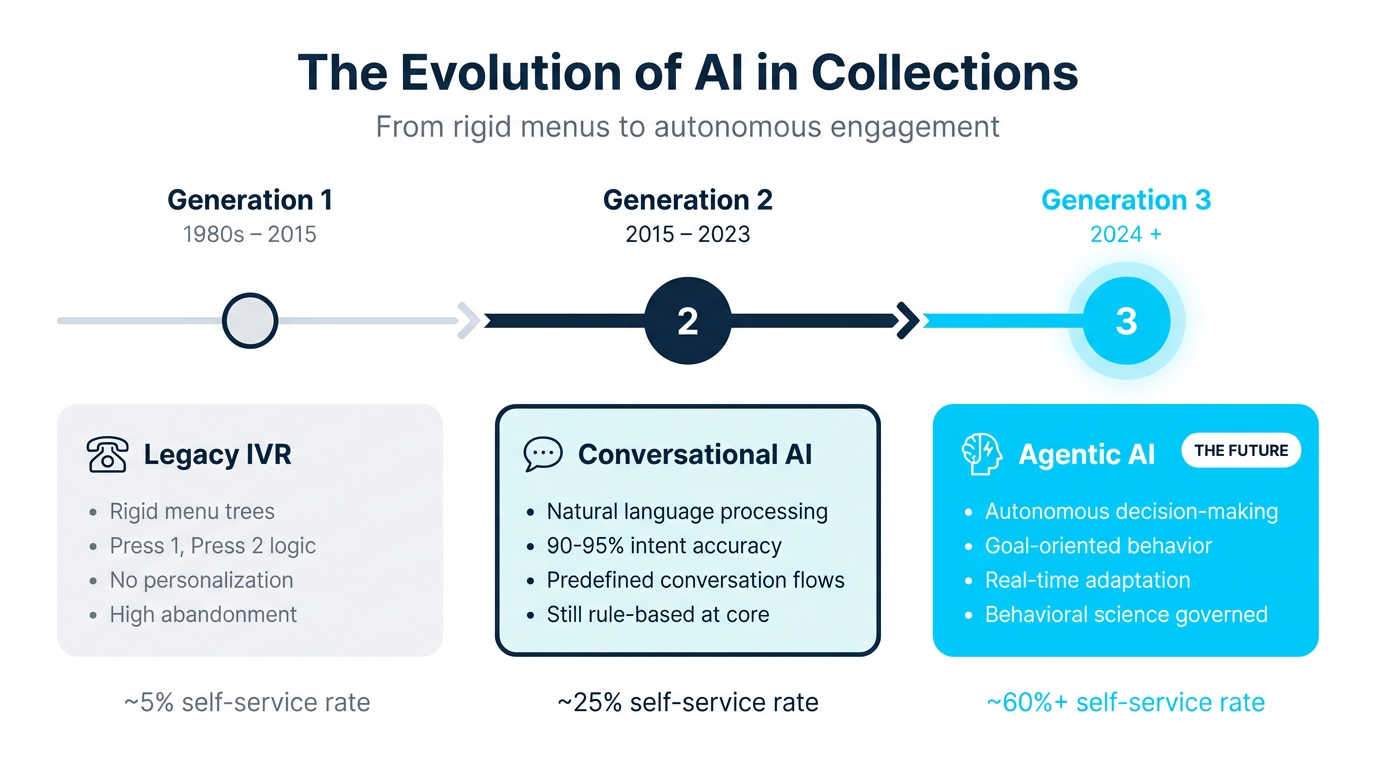

3 Generations of AI in Collections

Understanding where the industry has been helps evaluate where it's going. AI in collections has evolved through three distinct generations:

Generation 1: Rules-Based Automation (Pre-2015)

Rigid IVR systems and rules-based workflows. "Press 1 for balance, Press 2 to pay." Every path was predefined. Self-service rates hovered around 5%. Customers who didn't fit the menu simply fell through.

Generation 2: Conversational AI (2015–2023)

Natural language processing enabled genuine two-way conversations. Systems could understand intent, respond contextually, and guide customers toward resolution. Self-service resolution rates jumped to 60%+, and organizations could operate effectively across time zones and languages without proportional agent scaling.

Generation 3: Agentic AI (2023–Present)

The current frontier. Agentic AI doesn't just respond — it initiates, strategizes, and adapts. These systems autonomously identify at-risk accounts before they become delinquent, design personalized intervention strategies, execute multi-step engagement sequences, and learn from each interaction.

Each generation demanded a corresponding leap in governance. Agentic AI that makes autonomous decisions about customer engagement requires glass box explainability, not black box opacity. Read our deep dive on glass box vs. black box AI governance →

Real-World Results

These aren't projections. Organizations using AI-powered behavioral engagement platforms are seeing measurable results today:

26.6% Self-Cure Rate — Rifco

Rifco, a subprime and near-prime auto finance provider, achieved a 26.6% self-cure rate through behavioral science-driven messaging that motivated customers to resolve past-due balances via self-service digital channels — despite an 80% reduction in outbound call volume.

+60% Cure Rate Lift — Leading UK Credit Card Provider

A leading UK credit card provider processing 400K+ placements annually achieved a 60% cure rate lift by replacing legacy outbound dialing with Delinquency Archetype-driven digital engagement (email and SMS), alongside an 83% reduction in outbound calls.

85% Average Reduction in Agent Interactions

Across enterprise clients — driven by digital-first engagement strategies that reach past-due customers through the channels where they actually respond.

Up to 10% Higher Recovery Rates

Achieved by enterprise clients using behavioral science-driven collections engagement, compared to traditional rules-based approaches.

These results compound over time because AI continuously optimizes from outcomes. Traditional systems require manual strategy updates; AI platforms learn from every interaction and improve automatically.

5 Questions to Ask Your AI Collections Vendor

When evaluating AI debt collection software, these five questions separate genuine AI capabilities from marketing buzzwords:

-

Is your AI explainable (glass box) or opaque (black box)?

Can you trace exactly why the system recommended a specific action for a specific customer? Regulators increasingly require this. If the vendor can't explain their model's decisions, that's a compliance risk you'll inherit.

-

How does it handle regulatory compliance across jurisdictions?

Look for built-in guardrails for CFPB, FDCPA, TCPA, and state-level regulations. Ask how quickly the platform updates when regulations change. Manual compliance updates create dangerous gaps.

-

Does it segment by behavioral readiness, not just risk score?

Risk scoring tells you who might not pay. Behavioral segmentation tells you why they're not paying and how to motivate them. A customer with high capacity but low readiness needs a fundamentally different approach than one with low capacity but high willingness.

-

Does it continuously learn and optimize from outcomes?

Ask for evidence of automated experimentation, not just model retraining. The platform should be running micro-experiments across messages, timing, and channels — and automatically promoting what works.

-

What measurable results have similar clients in my industry achieved?

Ask for case studies with specific metrics — recovery rate improvements, cost reduction percentages, customer satisfaction scores — from organizations similar to yours in industry and scale. See real case studies here →

The Bottom Line

AI is rapidly becoming table stakes in collections. But the platforms that deliver sustained, compounding improvement are those built on behavioral science — not AI alone. Understanding why a customer isn't paying, and tailoring every interaction to their psychological state and financial circumstances, is what separates a 10x ROI from a one-time lift.

The right questions to ask any vendor aren't about feature lists. They're about science, governance, and proven outcomes. Organizations that get this right don't just recover more — they retain more customers and build the kind of trust that survives a difficult moment in a customer's financial life.

Ready to see what behavioral science-driven collections looks like in practice? Explore SymendCure or request a personalized demo.