Subprime Auto Loan Collections: How Behavioral Science Reduces Defaults and Improves Self-Cure Rates

Subprime auto delinquency hit a 32-year record in 2026. The lenders outperforming this market aren't the ones making more calls — they're the ones making smarter ones.

Key Takeaways

- Subprime auto delinquency (60+ days) hit 6.9% in January 2026 — a 32-year record, surpassing the Great Recession peak (Fitch Ratings).

- Average monthly car payments now exceed $748–$772, and nearly one in four new-car buyers now take 84-month terms — creating extended affordability exposure across the portfolio.

- Traditional volume-based outreach backfires in this environment: it assumes a motivation problem when most borrowers face a capacity problem.

- Rifco, a Canadian subprime auto lender, achieved a 26.6% self-cure rate and 80% reduction in outbound calls using behavioral archetype segmentation.

- The collections platforms winning in 2026 segment by capacity to pay and readiness to act — not just days past due or credit score.

Reducing subprime auto loan defaults requires knowing why a borrower stopped paying — not just that they did. Behavioral science platforms that classify borrowers by capacity to pay and readiness to act consistently outperform volume-based collections models. Rifco, a Canadian subprime auto finance company, achieved a 26.6% self-cure rate and 80% fewer outbound calls by replacing generic high-frequency outreach with behavioral archetype segmentation. The same approach that works for credit cards and telecom works for auto — but auto has distinct pressures that make it even harder to get right.

Why Subprime Auto Loan Collections Are Uniquely Hard

Auto loan collections sit in a peculiar middle ground. Unlike credit cards, the vehicle is essential transportation — most subprime borrowers have strong intrinsic motivation to cure, because losing the car means losing access to work, childcare, and daily life. Unlike mortgages, the asset depreciates rapidly, making repossession a costly outcome for the lender even when it succeeds.

That motivation should make collections easier. In practice, it often makes it harder. Borrowers who feel pressured on an asset they desperately need tend to avoid contact rather than engage. A high-frequency call campaign — the standard playbook — triggers anxiety and avoidance in exactly the population most likely to self-cure given the right support.

Compound this with the 2026 affordability environment. Subprime 60+ day delinquency reached 6.9% in January 2026 — a 32-year record. Average new-car monthly payments now range from $748–$772, and nearly one in four new-car buyers now choose 84-month terms in an attempt to bring payments within reach. The borrowers most at risk aren't bad actors. They're people who took on payment obligations that made sense at purchase and no longer fit their budget after years of elevated costs.

"The borrowers behind today's subprime auto delinquency numbers mostly want to pay. They need a frictionless path and an empathetic message — not another call that makes them feel worse about a situation they're already stressed about."

The Missing Layer: Why Credit Score Alone Isn't Enough

Traditional auto loan collections relies heavily on risk scoring to prioritize who to call — ranking past-due accounts by probability of recovery and directing agent effort accordingly. Risk scoring answers an important question: who is most likely to pay? It doesn't answer the harder question: how do I engage them in a way that actually motivates action?

Two borrowers with identical credit scores and identical days-past-due can have completely different reasons for non-payment — and completely different responses to the same outreach. One has the cash available but hasn't prioritized the payment. Another has restructured their budget around a job loss and genuinely can't pay the full balance this month. A third has disengaged from the lender after a prior collections interaction that felt adversarial.

Generic outreach handles all three identically. Behavioral science handles each differently — because the intervention that resolves one archetype actively pushes another toward charge-off. As we explored in our analysis of why predictive AI alone isn't enough for delinquency management, the missing layer is behavioral segmentation that answers why and how, not just who.

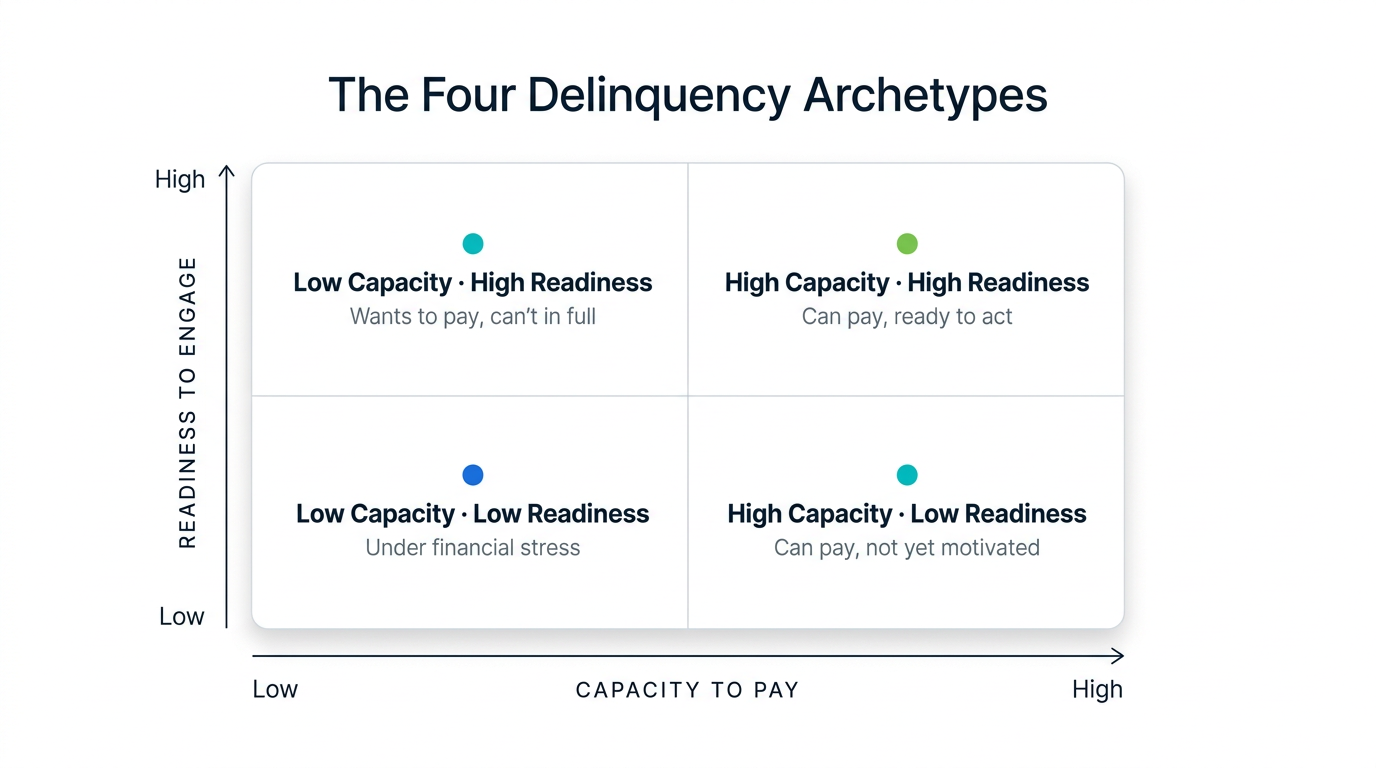

Delinquency Archetypes in Auto Finance

Symend's delinquency archetype model classifies past-due borrowers across two dimensions: their capacity to pay (financial ability) and their readiness to act (behavioral motivation). The result is four distinct groups, each requiring a fundamentally different collections approach.

Symend segments past-due borrowers by capacity and readiness — not just days past due or credit score.

In auto finance, each archetype looks distinct:

- High Capacity, High Readiness: Has the funds and wants to resolve. Needs a fast, friction-free digital payment path — not a call. Any friction in the resolution process is a missed self-cure.

- High Capacity, Low Readiness: Can pay but hasn't prioritized the account. Needs a message that creates urgency without pressure — loss aversion framing, a clear deadline, a low-effort action. Repeated calls here rarely work and often backfire.

- Low Capacity, High Readiness: Wants to resolve but genuinely can't pay in full. Needs flexible payment options, honest acknowledgment of their situation, and a path that feels achievable — not a demand for the full balance.

- Low Capacity, Low Readiness: Under significant financial stress and disengaged. Needs early, empathetic outreach before the gap widens — not escalation. This is the cohort where early intervention costs least and matters most.

A collections strategy that can't distinguish these four groups will over-call the High Capacity accounts (eroding the relationship) and under-support the Low Capacity ones (accelerating charge-off). Archetype segmentation fixes both failure modes simultaneously.

How Behavioral Science Improves Auto Loan Collections: A 5-Step Framework

The behavioral science approach to auto loan collections isn't a single tactic — it's a systematic framework that replaces volume-based outreach with outcome-optimized engagement.

Ingest behavioral signals beyond credit score

Effective archetype classification draws on 100+ real-time behavioral and engagement signals — payment history patterns, channel responsiveness, prior engagement timing, life event indicators — not just credit score and days past due. The richer the signal, the more accurate the archetype assignment.

Classify each borrower by archetype at account entry

As soon as an account enters delinquency, assign it to a behavioral archetype. Early classification enables early intervention — the most cost-effective point in the collections funnel. Waiting for 60+ DPD before segmenting loses most of the High Readiness population to self-cure or charge-off.

Select channel, message, and timing by archetype

High Capacity, High Readiness borrowers respond to digital push notifications with a one-tap payment link. High Capacity, Low Readiness borrowers respond to loss aversion messaging with a clear resolution deadline. Low Capacity borrowers need empathetic messaging and flexible options — not urgency framing. Same DPD, completely different playbook.

Remove friction from the resolution path

Every step between a borrower's intent to pay and the payment itself is an opportunity for abandonment. Archetype-optimized outreach doesn't just improve the message — it pre-builds the path. Deep links directly to payment portals, pre-filled account details, and mobile-first design all measurably improve completion rates in the High Readiness population.

Optimize continuously from real-world outcomes

Archetype assignments aren't static. As borrower behavior reveals new signals, the model updates — moving accounts between archetypes as their capacity or readiness changes. The result is a collections system that improves over time rather than degrading as market conditions shift.

Case Study: How Rifco Achieved a 26.6% Self-Cure Rate

Rifco is a Canadian subprime auto finance company operating in one of the most challenging segments of the auto lending market. When subprime delinquency rates began climbing, Rifco faced a familiar problem: a high-volume outbound collections operation that was generating agent cost without proportionally generating cures. The borrowers they most needed to reach were also the ones most likely to avoid contact when pressure increased.

Working with Symend, Rifco replaced its generic outreach model with behavioral archetype segmentation — using behavioral signals to classify each past-due account and deliver channel- and message-optimized engagement at the archetype level rather than the portfolio level.

The results redefined what their collections operation looked like:

| Metric | Result |

|---|---|

| Self-cure rate | 26.6% |

| Reduction in outbound calls | −80% |

| Direct phone/email response rate | 34% |

| Agent capacity redirected to complex accounts | Significant |

The 26.6% self-cure rate is the headline — but the 80% reduction in outbound calls is the structural change. Rifco didn't just improve outcomes. It changed the economics of its collections operation: fewer calls, more self-service resolutions, and agent capacity freed up for the genuinely complex accounts that benefit from human engagement. The full story is in the Rifco case study.

"A 26.6% self-cure rate means more than one in four past-due borrowers resolved without agent involvement — at near-zero marginal cost per cure. That's what behavioral segmentation looks like at scale."

Five Metrics Auto Finance Leaders Should Track

Most auto loan collections dashboards optimize for contact rate and right-party contact rate. These are proxies — inputs to collections, not outcomes. The metrics that actually reveal whether a behavioral approach is working are different:

- Self-cure rate: The share of past-due accounts that resolve without direct agent intervention. A rising self-cure rate is the clearest signal that digital engagement strategy is working. Target: 20%+ for a well-implemented behavioral program.

- Archetype accuracy: How often a borrower's actual behavior matches the predicted archetype response. High accuracy means the model is well-calibrated; mismatches reveal where signal data needs enrichment.

- Cost per cure by channel: Digital self-cure costs a fraction of agent-assisted cure. Tracking this by channel and archetype reveals where automation should expand and where human touchpoints still add value.

- Cure rate by archetype: Which archetype-specific playbooks are working, which need adjustment, and how the portfolio is shifting between archetypes over time. This is where model optimization happens.

- Post-cure delinquency recurrence: The percentage of cured accounts that fall past due again within 90 days. High recurrence rates often reflect underlying income fragility that a cure alone doesn't address. SymendPrevent provides bill-payment protection for cured customers — covering their bills if a qualifying income-disruption event (job loss, illness, disability, or death) occurs, reducing the likelihood they re-enter delinquency due to an involuntary event.

The Path Forward for Auto Finance Leaders

The subprime auto loan market in 2026 doesn't reward the lenders with the highest call volume. It rewards the ones who can identify which borrowers will self-cure with the right digital nudge, which need empathetic agent support, and which need flexible payment options — and then deliver each of those experiences without conflating them.

Rifco proved this is achievable in a subprime portfolio. The behavioral science approach that cut their outbound calls by 80% and pushed their self-cure rate to 26.6% is built on a proven, repeatable framework — one calibrated to each lender's portfolio and data, but grounded in the same archetype methodology available to enterprise auto finance lenders.

The underlying economics are compelling. A self-cure costs near zero in marginal agent time. An agent-assisted cure costs multiples more. A charge-off, even with repossession, rarely returns full value on a depreciated asset. In a market where 6.9% of subprime borrowers are 60+ days past due, shifting even 5–10 percentage points of that population toward self-cure transforms the P&L of a collections operation — without adding headcount or technology complexity.

See how behavioral science transforms auto loan collections

Explore Symend's approach to subprime auto delinquency — archetype segmentation, self-cure optimization, and post-cure protection that holds your portfolio together.

AUTO FINANCING SOLUTION REQUEST A DEMO