Credit Card Collections: How Behavioral Science Reduces Charge-offs and Improves Self-Cure Rates

US credit card delinquency hit a 15-year high in 2026. Card issuers that outperform aren’t sending more messages — they’re sending better ones.

Key Takeaways

- US credit card delinquency hit a 15-year high in 2026, with Canada and the UK following the same trajectory.

- Credit cards are the hardest asset class to collect: unsecured, revolving, high-volume, low-margin — and aggressive outreach destroys the long-term customer relationship.

- Traditional volume-based collections treats as a motivation problem what is often a capacity problem — or vice versa — producing suboptimal outcomes for both.

- A major UK credit card provider achieved a 60% improvement in cure rates and £40M in digital-channel recovery — while cutting outbound calls by 83%.

- The collections platforms winning in 2026 segment cardholders by capacity to pay and readiness to act — not just days past due or credit score.

Reducing credit card charge-offs requires understanding why a cardholder stopped paying — not just that they did. Behavioral science platforms that classify cardholders by capacity to pay and readiness to act consistently outperform volume-based collections models in unsecured lending. A major UK credit card provider working with Symend achieved a 60% improvement in cure rates and £40M in digital-channel recovery — while cutting outbound call volume by 83%. The same archetype methodology that works for auto finance and telecommunications applies directly to credit cards — but the unsecured, revolving nature of the product creates distinct pressures that make behavioral precision even more critical.

Why Credit Card Collections Is the Hardest Asset Class

Every credit portfolio has a collections challenge. Credit card collections is uniquely difficult because of four compounding factors that don’t apply to secured lending in the same way:

No collateral, no backstop. Unlike auto loans or mortgages, credit card debt is unsecured. Card issuers have limited structural leverage — no asset to repossess, no property to foreclose. The only mechanisms are credit reporting, legal action, and persistent outreach. Of these, persistent outreach is the only one that preserves the relationship, and it only works when it’s calibrated to the cardholder’s actual situation.

The revolving relationship problem. A cardholder who feels harassed by their card issuer doesn’t just become harder to collect from — they become a churned customer. The long-term economic value of a credit card account depends on the cardholder continuing to use and maintain the product after the delinquency resolves. Collections tactics that win a short-term payment while destroying the relationship produce a net negative outcome at the portfolio level.

Volume and margin pressure. Credit card issuers manage millions of accounts across a wide spectrum of risk tiers. The margin per account is thin relative to mortgages or auto loans, which makes cost-per-cure economics a primary lever. Sending 10 agent calls to recover a £200 balance destroys unit economics. The business case for digital self-cure and behavioral automation is stronger in credit cards than in almost any other asset class.

Regulatory scrutiny. Regulators in the US (CFPB), UK (FCA Consumer Duty), and Canada (FCAC) have all intensified scrutiny on collections practices in recent years. Card issuers must demonstrate good outcomes for customers in financial difficulty — not just compliant process. That shift from process compliance to outcome demonstration requires a fundamentally different engagement model, one that can show regulators that each intervention was proportionate to the cardholder’s actual situation.

“The cardholders behind today’s credit card delinquency numbers aren’t mostly bad actors. They’re people in a range of different situations — some who have the funds and haven’t acted, some who genuinely can’t pay right now, and some who have disengaged entirely. Treating them identically is what drives charge-offs.”

The Missing Layer: Why Risk Scoring Alone Fails

Traditional credit card collections relies heavily on risk scoring to prioritize outreach — ranking past-due accounts by probability of recovery and directing agent effort accordingly. Risk scoring answers an important question: who is most likely to pay? It doesn’t answer the harder question: how do I engage them in a way that actually motivates action?

Two cardholders with identical credit scores and identical days-past-due can have completely different reasons for non-payment — and completely different responses to the same outreach. One missed their autopay after switching bank accounts and has the full balance ready to transfer. Another has restructured their budget around a job loss and genuinely can’t pay the minimum this month. A third has disengaged entirely after a prior collections interaction that felt adversarial and shame-inducing.

Generic outreach handles all three identically. Behavioral science handles each differently — because the intervention that resolves one archetype actively pushes another toward charge-off. As we explored in our analysis of why predictive AI alone isn’t enough for delinquency management, the missing layer is behavioral segmentation that answers why and how, not just who.

This is especially acute in credit cards because the “shame signal” is strong. Research consistently shows that credit card debt carries a higher emotional burden than secured debt — partly because it’s associated with consumption choices rather than asset acquisition. Cardholders in the Low Capacity archetypes are particularly prone to avoidance behavior when outreach feels accusatory. High-frequency pressure tactics accelerate avoidance exactly when engagement is most needed.

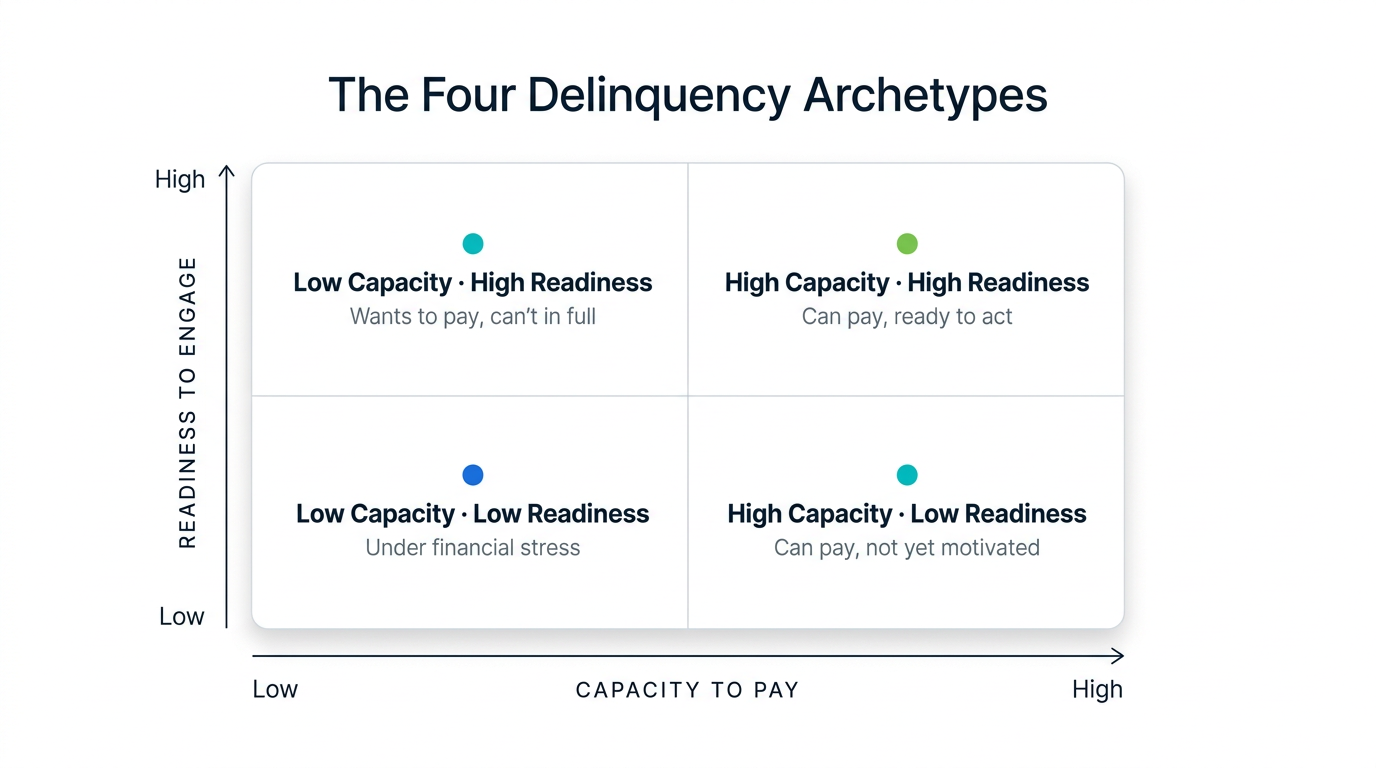

Delinquency Archetypes in Credit Card Collections

Symend’s delinquency archetype model classifies past-due cardholders across two dimensions: their capacity to pay (financial ability) and their readiness to act (behavioral motivation). The result is four distinct groups, each requiring a fundamentally different collections approach.

Symend segments past-due cardholders by capacity and readiness — not just days past due or credit score.

In a credit card portfolio, each archetype presents differently:

- High Capacity, High Readiness: Has the funds and intends to resolve — may have simply forgotten, missed an autopay update, or let a busy week slide. Needs a single friction-free digital payment link. Any unnecessary steps in the resolution path are a missed self-cure opportunity.

- High Capacity, Low Readiness: Can pay but has deprioritized the account. Responds to loss aversion framing — clear articulation of credit score impact, a deadline, a low-effort resolution path. Repeated calls rarely convert this group; they harden resistance and increase avoidance.

- Low Capacity, High Readiness: Wants to resolve but genuinely cannot pay the full balance right now. Needs flexible minimum payment options, an empathetic tone, and a path that acknowledges their situation — not a demand for the full balance that they can’t meet.

- Low Capacity, Low Readiness: Under financial stress and disengaged from communication. Needs early, low-pressure outreach that opens a channel before the gap widens — not escalation that reinforces avoidance. This is the cohort where early intervention costs least and matters most.

A collections strategy that can’t distinguish these four groups will over-contact the High Capacity accounts (eroding the relationship and triggering avoidance) and under-support the Low Capacity ones (accelerating charge-off). Archetype segmentation fixes both failure modes simultaneously — often while reducing total outreach volume significantly.

How Behavioral Science Improves Credit Card Collections: A 5-Step Framework

The behavioral science approach to credit card collections isn’t a single tactic — it’s a systematic framework that replaces volume-based outreach with outcome-optimized engagement.

Ingest behavioral signals beyond credit score

Effective archetype classification draws on 100+ real-time behavioral and engagement signals — payment history patterns, channel responsiveness, prior engagement timing, life event indicators, digital interaction data — not just credit score and days past due. In credit card portfolios, digital engagement signals are particularly rich: app login frequency, statement view patterns, and prior self-cure behavior all carry predictive value that credit scores miss entirely.

Classify each cardholder by archetype at account entry

As soon as an account enters delinquency, assign it to a behavioral archetype. Early classification enables early intervention — the most cost-effective point in the collections funnel. In credit cards, waiting until 60+ DPD to segment loses most of the High Readiness population to self-cure or charge-off; the window for low-cost intervention is narrow in the early delinquency cycle.

Select channel, message, and timing by archetype

High Capacity, High Readiness cardholders respond to a single push notification with a one-tap payment link. High Capacity, Low Readiness cardholders respond to loss aversion messaging with a clear resolution deadline and credit score framing. Low Capacity cardholders need empathetic messaging, flexible minimum payment options, and no urgency framing. Same DPD, completely different playbook — and the same rule applies across digital, SMS, email, and agent channels.

Remove friction from the resolution path

Every step between a cardholder’s intent to pay and the payment itself is an opportunity for abandonment. Archetype-optimized outreach pre-builds the resolution path: deep links directly to payment portals, pre-filled account details, and mobile-first design all measurably improve completion rates in the High Readiness population. In credit cards, where many cardholders have the funds but not the motivation, friction reduction alone drives meaningful self-cure rate improvement.

Optimize continuously from real-world outcomes

Archetype assignments aren’t static. As cardholder behavior reveals new signals, the model updates — moving accounts between archetypes as their capacity or readiness changes. A cardholder who was Low Capacity in month one and receives a paycheck in month two is now a different engagement target. The result is a collections system that adapts to real-world circumstances rather than locking a cardholder into a classification made at account entry.

Case Study: Major UK Credit Card Provider — 60% Cure Lift and £40M Digital Recovery

One of the UK’s leading credit card providers faced a structural collections problem familiar to every large card issuer: a high-volume outbound operation generating significant agent cost, with cure rates that plateaued despite continued investment in contact capacity. The cardholders they most needed to reach were also the ones most likely to avoid contact under pressure — and the ones most likely to churn if the collections experience felt adversarial.

Working with Symend, the issuer replaced portfolio-level outreach with behavioral archetype segmentation. Using 100+ real-time behavioral and engagement signals, each past-due account was classified at entry and engaged through the channel, message, and timing most likely to drive resolution for that specific archetype. Digital channels became the primary cure vehicle for the High Readiness population; agent capacity was redirected toward the Low Capacity archetypes where human engagement adds genuine value.

The results transformed both their collections economics and their customer outcomes:

| Metric | Result |

|---|---|

| Improvement in cure rates | +60% |

| Reduction in outbound call volume | −83% |

| Recovery through digital channels | £40M |

| Agent capacity redirected to complex accounts | Significant |

The 60% improvement in cure rates is the headline — but the 83% reduction in outbound calls is the structural change. The issuer didn’t add capacity or headcount. It changed the economics of its collections operation: fewer calls, more self-service resolutions, and £40M collected through digital engagement. Agent capacity freed up by the digital shift was redeployed to the genuinely complex accounts where human judgment and empathy add irreplaceable value.

“Recovering £40M through digital channels — with 83% fewer outbound calls — means the cost-per-cure economics changed fundamentally. That’s what behavioral segmentation looks like at scale in a credit card portfolio.”

Five Metrics Credit Card Issuers Should Track

Most credit card collections dashboards optimize for contact rate and right-party contact rate. These are inputs — they don’t reveal whether the engagement strategy is actually changing behavior. The metrics that reveal whether a behavioral approach is working are different:

- Self-cure rate: The share of past-due accounts that resolve without direct agent intervention. A rising self-cure rate is the clearest signal that digital engagement strategy is working. In credit cards, where digital channel penetration is typically high, self-cure rates above 30% are achievable with well-implemented behavioral programs.

- Cure rate by archetype: Which archetype-specific playbooks are working, which need adjustment, and how the portfolio is shifting between archetypes over time. This is where model optimization happens — and where early indicators of changing cardholder behavior surface.

- Cost per cure by channel: Digital self-cure costs a fraction of agent-assisted cure. Tracking this by channel and archetype reveals where automation should expand and where human touchpoints still generate positive ROI. In credit card collections, the unit economics gap between digital and agent cure is particularly wide.

- Archetype accuracy: How often a cardholder’s actual behavior matches the predicted archetype response. High accuracy means the model is well-calibrated; mismatches reveal where signal data needs enrichment or where a segment is being systematically misclassified.

- Post-cure delinquency recurrence: The percentage of cured accounts that fall past due again within 90 days. High recurrence rates often reflect underlying income fragility that a cure alone doesn’t address. SymendPrevent provides bill-payment protection for cured customers — covering their bills if a qualifying income-disruption event (job loss, illness, disability, or death) occurs, reducing the likelihood they re-enter delinquency due to an involuntary event outside their control.

The Path Forward for Card Issuers

The credit card delinquency environment in 2026 doesn’t reward the issuers with the highest call volume. It rewards the ones who can identify which cardholders will self-cure with a single friction-free digital message, which need empathetic agent support and flexible payment options, and which are in genuine financial difficulty requiring early low-pressure intervention — and then deliver each of those experiences without conflating them.

A major UK credit card provider proved this is achievable at scale. The behavioral science approach that cut their outbound calls by 83% and recovered £40M through digital channels is built on a proven, repeatable framework — one calibrated to each issuer’s portfolio and data, but grounded in the same archetype methodology available to enterprise card issuers.

The underlying economics are compelling in credit cards more than in almost any other asset class. Digital self-cure costs near zero in marginal agent time. Agent-assisted cure costs multiples more. And in a market where delinquency has hit a 15-year high, the issuers that shift even a meaningful fraction of past-due accounts toward self-cure fundamentally transform their collections P&L — while improving the outcomes their regulators are now demanding as evidence of good customer treatment.

See how behavioral science transforms credit card collections

Explore Symend’s approach to credit card delinquency — archetype segmentation, digital self-cure optimization, and post-cure protection that holds your portfolio together.

FINANCIAL SERVICES SOLUTION REQUEST A DEMO