After the Cure: Why Cured Customers Still Churn — and How to Stop It

Every collections dashboard has a cure metric. Almost none have a post-cure retention metric — and that’s where the real value disappears.

Every collections team knows the feeling of a clean win: the past-due balance clears, the account flips back to current, and the case closes. The metric that mattered — the cure — is in the bank. So the team moves on to the next delinquent account.

And three months later, the customer they just recovered cancels their service.

This is customer churn after collections, and it’s the blind spot in nearly every collections ROI calculation. We measure how well we bring customers back from delinquency. We rarely measure whether they stay. This post breaks down why cured customers leave, why your current ROI math doesn’t see it, and what it takes to turn a cure into a retained, paying relationship.

What is customer churn after collections?

Customer churn after collections is when a customer resolves a past-due balance — they “cure” — but then leaves the business shortly afterward, either by cancelling (voluntary churn) or by falling back into delinquency and being written off or disconnected (involuntary churn). The recovery is recorded as a success, but the customer is lost anyway.

The cure is a milestone, not a finish line

Collections has spent a decade getting better at the recovery itself. Behavioral science and AI have pushed cure rates up and cost-to-collect down. Symend alone has treated more than 250M delinquencies and recovered over $50B in payments for enterprise clients.

But “recovered” and “retained” are not the same word. A customer can pay you on Tuesday and leave you on Friday. When that happens, the balance you fought to recover comes with an expiration date — and the lifetime value you assumed you’d protected walks out the door with the customer.

The reason this slips through is structural. Collections is scored on cures. Retention is scored on churn. Those numbers usually live in different teams, different dashboards, and different quarterly reviews. So the customer who cures and then leaves is counted as a win in one system and a loss in another — and nobody connects the two.

Two kinds of post-cure churn

Once you look for it, post-cure churn splits cleanly into two types, and they have very different causes and fixes.

Voluntary churn: the relationship got damaged

The first type is the customer who could stay but chooses not to. They paid what they owed, but the experience of being collected from left a mark. Aggressive calls, generic threats, and high-frequency pressure recover the balance while quietly eroding the relationship behind it. The customer cures, then leaves the first chance they get — often for a competitor.

This is collections-driven churn, and it’s entirely self-inflicted. It’s the predictable cost of treating delinquency as an enforcement problem rather than a relationship moment.

Involuntary churn: the next shock hit

The second type is the customer who wants to stay but can’t. They cured once, then a real-life event — a job loss, an illness, a disability — knocked them back into delinquency. This time there’s no recovery. The account ages out, gets written off, and the service is disconnected.

This is involuntary churn: the customer doesn’t decide to leave, circumstances decide for them. And it’s rising. According to the Federal Reserve Bank of New York’s Survey of Consumer Expectations, the share of consumers who expect to miss a debt payment in the next three months is at its highest point since 2020, and the rate of missed payments has climbed roughly 46% over five years. Many of the customers you cure this quarter are one bad month away from being delinquent again.

Consumers’ expectation of missing a debt payment in the next three months is at its highest level since 2020 — meaning a meaningful share of every cured cohort is already at risk of relapsing.

Source: Federal Reserve Bank of New York, Survey of Consumer Expectations.

Why your ROI math doesn’t see it

Most collections ROI models stop calculating at the moment of cure. Dollars recovered, minus cost to recover, equals return. Clean and defensible — and incomplete.

What that model leaves out is the line item underneath: how much of the recovered value actually survives. A cure that’s followed by churn 90 days later isn’t a full recovery; it’s a deferred loss with a one-quarter delay. When you re-run the math with retention included, two collections programs that look identical on cure rate can produce wildly different real returns.

“A cure followed by churn isn’t a recovery. It’s a deferred loss with a one-quarter delay.”

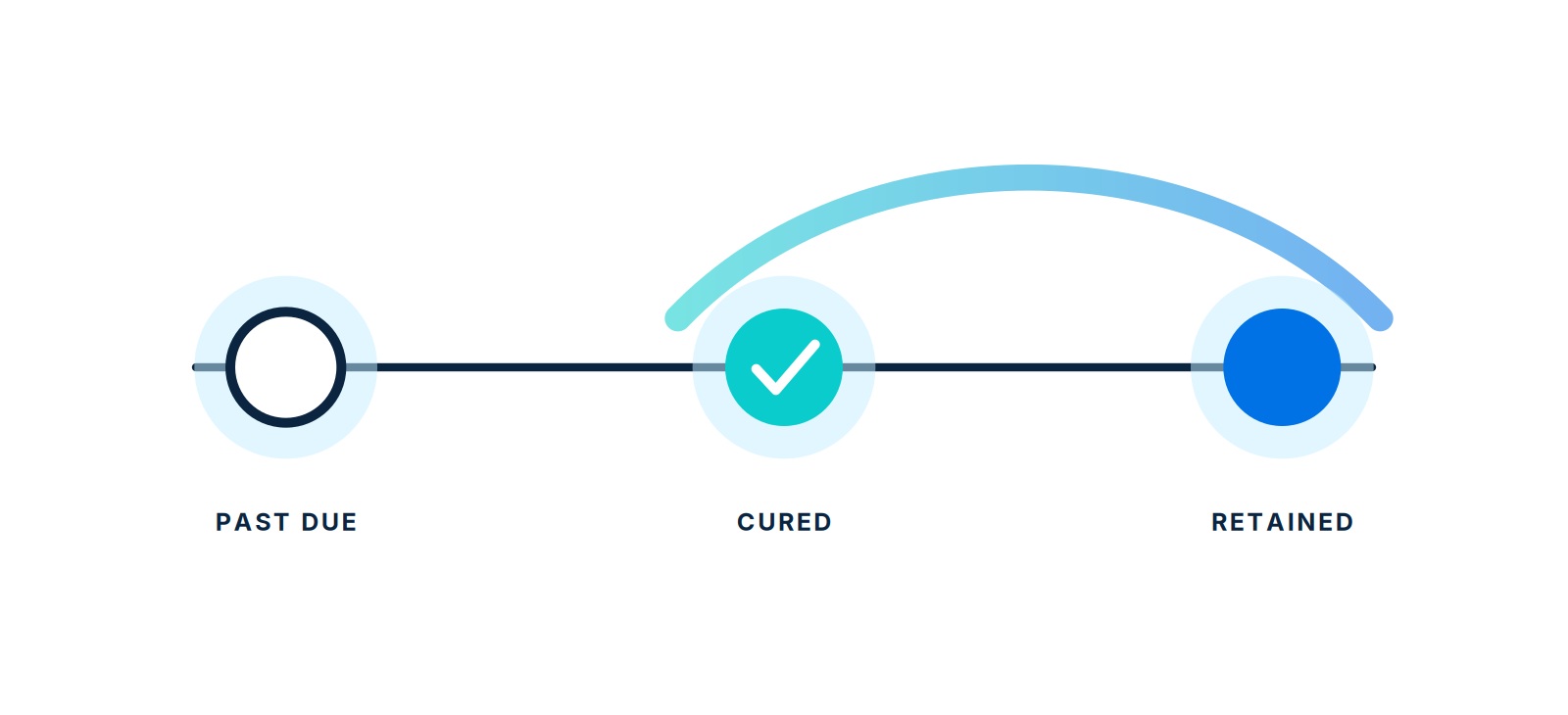

The fix isn’t a better spreadsheet. It’s treating the cure as the start of a retention window, not the end of a collections case — and building for both kinds of post-cure churn deliberately.

How to stop it, part 1: cure in a way customers want to come back from

You can’t retain a customer you alienated during recovery. So the first lever is the collections experience itself.

This is where the difference between AI alone and behavioral science paired with AI shows up most clearly. AI-only tools optimize for the next payment. Behavioral science optimizes for the next payment and the relationship that produces the one after it — by reading where a customer actually is and meeting them with the right tone, timing, and channel instead of a generic pressure sequence.

Symend’s behavioral science–driven collections engagement is built on exactly this idea: identify the “willing but stretched” customer early and connect them to a supportive path rather than a punitive one. The results follow the relationship, not just the balance. TELUS increased digital interactions with past-due customers by 220% in under four months — engagement that recovers the debt while strengthening the relationship rather than spending it. Symend’s telecom programs have been associated with a 30% reduction in voluntary churn, alongside the platform’s documented 10x ROI and up to 10% higher recovery rates.

For banks, lenders, and card issuers, where switching costs are low and a single bad collections experience can end a multi-product relationship, this empathy-first approach is the difference between recovering an account and keeping a customer.

How to stop it, part 2: protect the cure against the next shock

Curing a customer with empathy solves voluntary churn. It does nothing for the customer who relapses because they lost their job. To address involuntary churn, you have to protect the cure itself — proactively, before the next income disruption hits.

That’s the gap SymendPrevent is built to close. SymendPrevent is a Bill Payment Protection solution that offers cured customers coverage for up to six months of bills in the event of job loss, critical illness, disability, or death. (Coverage is provided by licensed insurers; Symend doesn’t underwrite or issue it.) When a covered customer is hit by a life event, claim payouts cover the bills — so the customer stays current instead of relapsing, and the business directly offsets bad debt instead of writing it off.

The behavioral science is in the timing. The offer is presented right after a customer cures — the exact moment their financial awareness is heightened and their motivation to protect themselves is highest. That’s not a coincidence; it’s the same understanding of customer psychology that drives engagement, applied to retention. A protection offer that would be ignored at signup gets meaningful uptake immediately after a delinquency scare.

“The best moment to protect a customer from the next delinquency is the moment they’ve just survived the last one.”

Two more things make this practical at enterprise scale. First, it ties the customer more tightly to your brand — embedded protection is a benefit they’d lose by leaving, which increases stickiness. Second, it runs as an easy add-on with zero cost, zero risk, and zero IT lift: Symend manages outreach, enrollment, claims, and support end-to-end, so there’s no added load on your call centers. For high-volume telecom and utility accounts that cycle through delinquency repeatedly, that turnkey model matters as much as the protection itself.

The retention dividend

Put the two levers together and the collections function changes shape. Instead of a cost center that recovers balances and quietly leaks customers out the back, it becomes a retention engine: customers are recovered in a way that preserves the relationship, then protected against the shock that would have ended it.

That’s the line item missing from the standard ROI calculation — and it’s the one that compounds. Every cured customer you also retain keeps generating revenue long after the recovered balance is forgotten. You can see the pattern across Symend’s documented client outcomes: the programs that win aren’t just curing more accounts, they’re keeping the customers behind them.

The cure was never the goal. A paying, retained customer is. Customer churn after collections is the gap between those two things — part of it self-inflicted by how we collect, part of it driven by life events we can actually protect against. Close both, and a recovered balance becomes a recovered relationship.

See how cured customers can become retained ones

Explore how SymendPrevent turns the post-cure moment into lasting retention — or request a custom report on the recovery, retention, and OpEx impact for your portfolio.

SYMENDPREVENT REQUEST A DEMO