How to Improve Debt Collection Recovery Rates: The Behavioral Playbook

Most advice on how to improve debt collection recovery rates comes down to doing more of the same thing harder: more calls, faster escalation, tighter cut-offs by days past due. It moves the number for a quarter or two, then plateaus. The reason it plateaus is that volume and escalation treat every past-due account as the same problem, when the accounts in any delinquent portfolio are not the same problem at all.

This article lays out a different approach — one built on behavioral science rather than on cadence. You'll learn why segmenting customers by why they aren't paying outperforms segmenting by how long they haven't paid, the specific levers that move recovery rates without adding outbound pressure, and the outcomes enterprise lenders and carriers have seen when they make the shift.

Why the standard recovery playbook stalls

The conventional path to higher recovery rates is well worn. Add agents. Increase call frequency. Escalate sooner. Segment the book into 30-, 60-, and 90-day buckets and apply a heavier touch as accounts age. Each lever produces a short-term lift, and then returns flatten — often while cost-to-collect keeps climbing.

The ceiling is structural. Outbound pressure assumes the barrier to payment is awareness or urgency, so the fix is to reach customers more often and more firmly. But for most past-due customers, awareness is not the problem. Symend's data shows that 78% of outbound collection calls are blocked or ignored, and fewer than 20% of customers are actually reached. Sending more messages into that environment doesn't change the recovery rate; it changes the cost of the recovery rate.

78%

of outbound collection calls are blocked or ignored — which is why adding volume rarely moves the recovery rate

There's also a quieter cost to leaning on volume. Every additional contact carries an operational price, and beyond a point it carries a relationship price too: the customers most worth retaining are often the ones most alienated by repetitive, escalating outreach. For a first-party creditor, a recovered balance that comes at the expense of a churned customer is a partial win at best.

Days past due, the axis the whole playbook is organized around, is the deeper issue. It measures elapsed time, not behavior. Two accounts sitting at 45 days past due can represent opposite situations: one customer has the money and simply needs a clear path to pay, while another is overwhelmed by financial stress and grows less likely to engage with every escalating contact. Treat them identically and you get a suboptimal result for both — and you leave recovery on the table.

The behavioral reframe: capacity to pay vs. readiness to act

The more useful question isn't "how late is this account?" It's "what is actually preventing this customer from paying, and what would move them to act?" Behavioral science research on payment psychology points to two independent dimensions that answer it: capacity to pay — whether the customer has the financial means — and readiness to act — whether they are psychologically prepared and motivated to engage.

These two axes are independent. A customer can have the money but be avoidant, rationalizing, or complacent. Another can be genuinely stretched financially but highly motivated to resolve the debt. A single risk score can assign both the same probability of payment while telling you nothing about which engagement strategy will work — because the strategies that work for them are opposites.

Plotting capacity against readiness produces four behavioral profiles, the foundation of Symend's Delinquency Archetypes framework. Each profile is driven by a different psychological mechanism and requires a fundamentally different approach:

HCHR — can pay, wants to resolve

High Capacity, High Readiness customers are held up by uncertainty, not unwillingness. They want a clear statement of what they owe and a frictionless way to pay it. Give them a single, direct path to resolution and they self-cure with minimal prompting. Over-engaging them — multi-step journeys, repeated follow-up — spends money without improving the outcome.

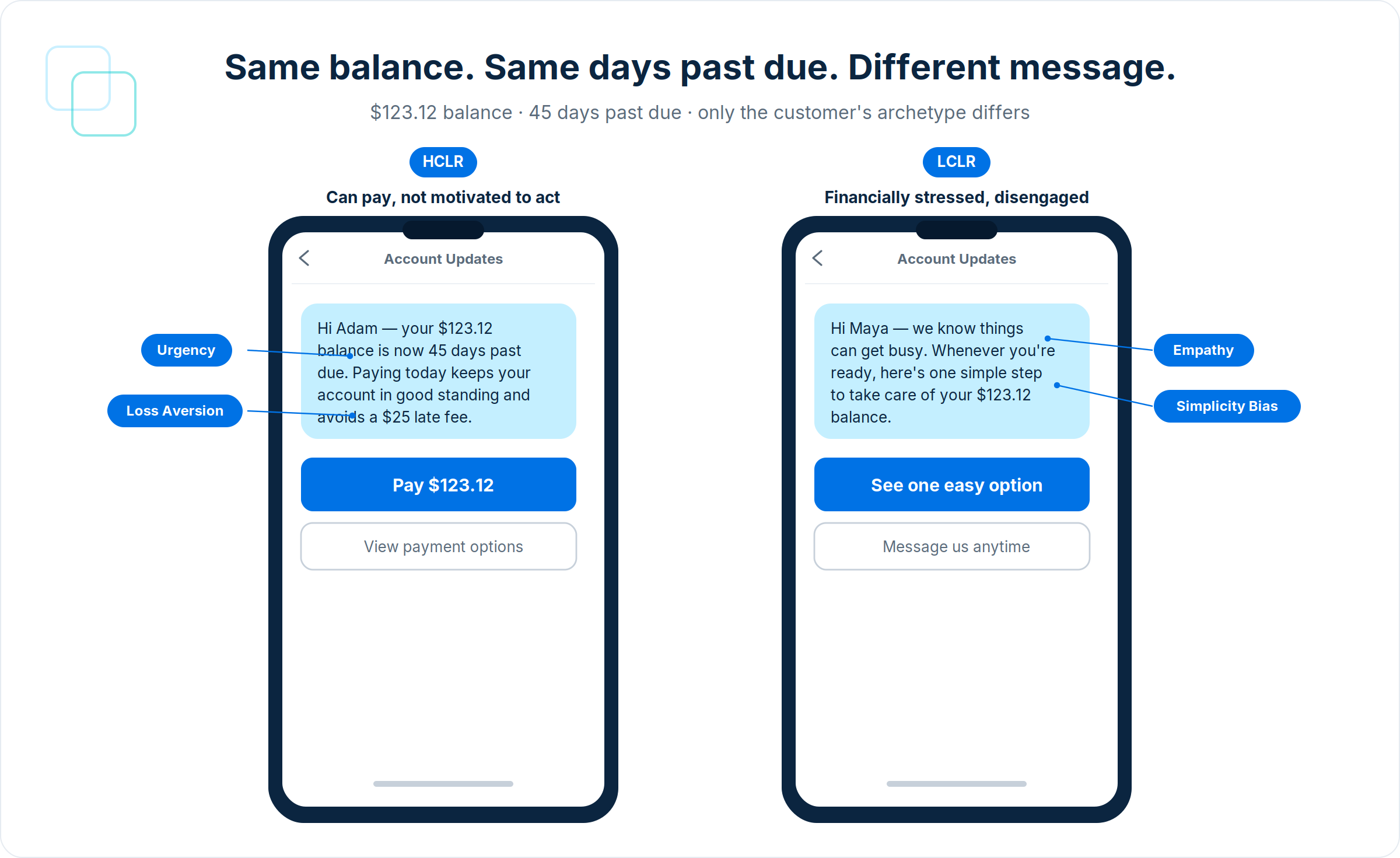

HCLR — can pay, not motivated to act

High Capacity, Low Readiness customers have learned, through repeated late payments without real consequence, that delay is effectively cost-free. Generic reminders confirm that belief. What moves them is reframing what's actually at stake — credit standing, service continuity, the relationship — made concrete and proximate, with urgency that's behaviorally triggered rather than volume-based.

LCHR — wants to pay, can't in full

Low Capacity, High Readiness customers are motivated but financially constrained. They need an achievable path, not a full-balance demand. Flexible arrangements that feel meaningful but manageable, framing that affirms their effort, and recognition of small steps forward all convert intent into payment. Escalation only adds shame to an account that was already recoverable.

LCLR — financially stressed, disengaged

Low Capacity, Low Readiness customers are experiencing what behavioral scientists call tunneling: acute financial stress narrows cognitive bandwidth, making it harder to process options or initiate action even when the intent exists. Menus of choices and escalating volume make it worse. One simple, concrete next step — delivered with empathy and, ideally, before full delinquency — is what reaches them.

The competitive advantage here isn't access to AI; every platform has that now. It's knowing which mechanism is blocking payment on a given account and designing the engagement to address it precisely.

Five levers that actually move recovery rates

Once capacity and readiness are visible, the levers that improve recovery rates change shape. They stop being about reaching customers more and start being about reaching them more relevantly.

1. Behavioral segmentation, not just risk scoring

Risk scoring answers how likely a customer is to pay. Behavioral segmentation answers why they aren't and what will change it. Layering archetype classification on top of your existing risk model lets you route each account to the engagement strategy its behavioral profile actually calls for — frictionless paths for the capable-but-uncertain, urgency reframing for the complacent, flexible options for the constrained, simplicity for the overwhelmed. This is the single highest-leverage change, because every downstream lever depends on it.

2. Personalized, behaviorally-informed messaging

With profiles in place, message content can be tuned to the mechanism rather than the calendar. The same 60-day account gets a loss-aversion reframe if it's HCLR or an empathetic, single-action message if it's LCLR. Personalization here means matching tone, channel, timing, and the specific behavioral tactic to the customer — not inserting a first name into a template.

The distinction is concrete. A loss-aversion frame makes a specific, proximate stake vivid — what the customer stands to lose by waiting — and works on the complacent customer who has stopped registering consequences. The same message sent to an overwhelmed, financially stressed customer backfires, adding pressure to someone whose cognitive bandwidth is already maxed out; for them, a single clear next step framed without blame is what converts. Same balance, same days past due, opposite messages — and the recovery rate reflects the difference.

3. Digital-first engagement

Most past-due customers are easier to reach, and far cheaper to reach, through digital channels than through outbound calls — and digital lets the customer engage on their own terms, which matters enormously for avoidant and overwhelmed profiles. A digital-first model anchored in self-serve resolution lifts cure rates while pulling cost out of the operation, and it reserves agent time for the accounts where a human conversation genuinely changes the outcome.

4. Pre-delinquency intervention

The most recoverable LCHR and LCLR customers are the ones you engage before financial stress fully sets in. Acting on early-risk signals — before an account is technically past due — widens the window in which an empathetic, low-friction nudge can keep a customer in good standing. SymendPrevent applies the same archetype-driven model to pre-delinquent accounts, and retains cured customers who would otherwise slip back into the cycle through involuntary churn. For lenders, this is increasingly where the marginal recovery point lives; the same logic applies across financial services collections portfolios.

5. Continuous analytics and optimization

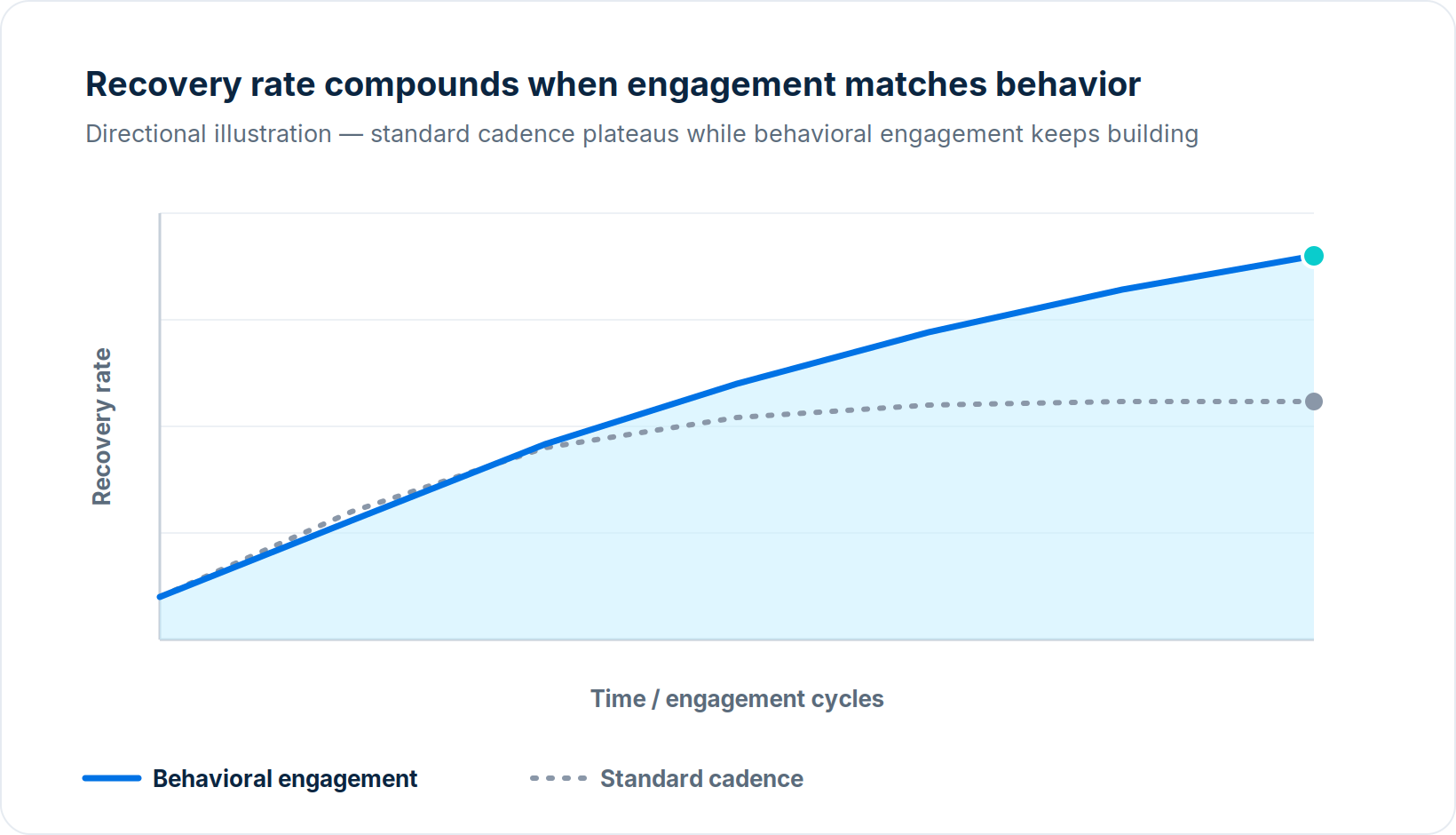

Behavioral engagement is not set-and-forget. Every interaction — opened, ignored, clicked, replied to — is a signal that should refine the next one. Real-time optimization of which tactic, channel, and timing works for which profile is what compounds results over time, turning a one-quarter lift into a sustained improvement in recovery rate and cost-to-collect.

This is also where a behavioral approach pulls away from a static one. A customer's profile is not fixed: an LCHR customer who completes a small arrangement is signaling movement; an HCHR account that stays silent past a frictionless prompt may be telling you the profile was misread. Engagement that reads those shifts and reclassifies in flight keeps treating each account as the customer it is now, not the one it was when the account first rolled past due — and that responsiveness is precisely what a fixed, days-past-due cadence cannot offer.

What behavioral engagement delivers

The shift from cadence to behavior produces measurable results across portfolios. SymendCure classifies each delinquent account by archetype and generates personalized outreach matched to the behavioral profile, and the outcomes follow the principle that effort concentrated where it changes behavior beats effort distributed evenly across every account.

Archetype-driven engagement outcomes

- 60%+ cure rate lift — a UK credit card provider, alongside £40M collected digitally and an 83% reduction in outbound calls

- 26.6% self-cure rate — Rifco auto finance, on digital-first, archetype-segmented engagement

- 85% reduction in agent interactions

- Up to 10% increase in overall recovery rates

- 220% increase in digital engagement — TELUS, while reducing OpEx by 50%

The telecommunications result is instructive: TELUS more than tripled digital engagement with past-due customers while taking cost out of the operation, because the gains came from relevance rather than reach. And the practitioner's-eye view of the change is worth more than any single number.

"Symend actually helped us see our collections strategy a little bit differently. We don't necessarily have to do the same thing at the same frequency on every account every day."

Tammy Shanks, Manager of Collections and Customer Service, Rifco

That's the whole reframe in one sentence. Improving recovery rates isn't about doing more on every account — it's about doing the right thing on each one. If you want the deeper methodology behind how capacity and readiness are modeled and applied, the predictive AI and behavioral science approach to delinquency management goes into the mechanics.

Where to start

You don't have to rebuild your collections operation to begin. Start by adding a behavioral lens to a single segment you already consider hard to recover — overlay capacity and readiness, match the engagement to the profile, and measure cure rate and cost-to-collect against your current approach. The accounts your standard playbook reaches least effectively are usually the ones behavioral engagement improves most.

Frequently Asked Questions

How to improve debt collection recovery rates

What is a good debt collection recovery rate

How does behavioral science improve collections recovery

What factors affect debt collection recovery rates

How to improve first-party collections recovery rates

How do you calculate a debt collection recovery rate

What is the difference between cure rate and recovery rate

Can digital-first collections improve recovery rates

Improve your recovery rates by changing the question

Higher recovery rates don't come from doing more to every account — they come from doing the right thing for each one. Segmenting on why customers aren't paying, matching engagement to the behavioral profile, and leading with digital-first, pre-delinquency intervention is what lifts recovery while lowering cost and protecting the customer relationship. The gains come from relevance, not pressure.

Talk to our team about a demo to see how archetype-driven engagement can improve recovery rates and reduce cost-to-collect across your portfolio.